.png)

.png)

Weekly Recap : Crypto Rates W43

Market Overview

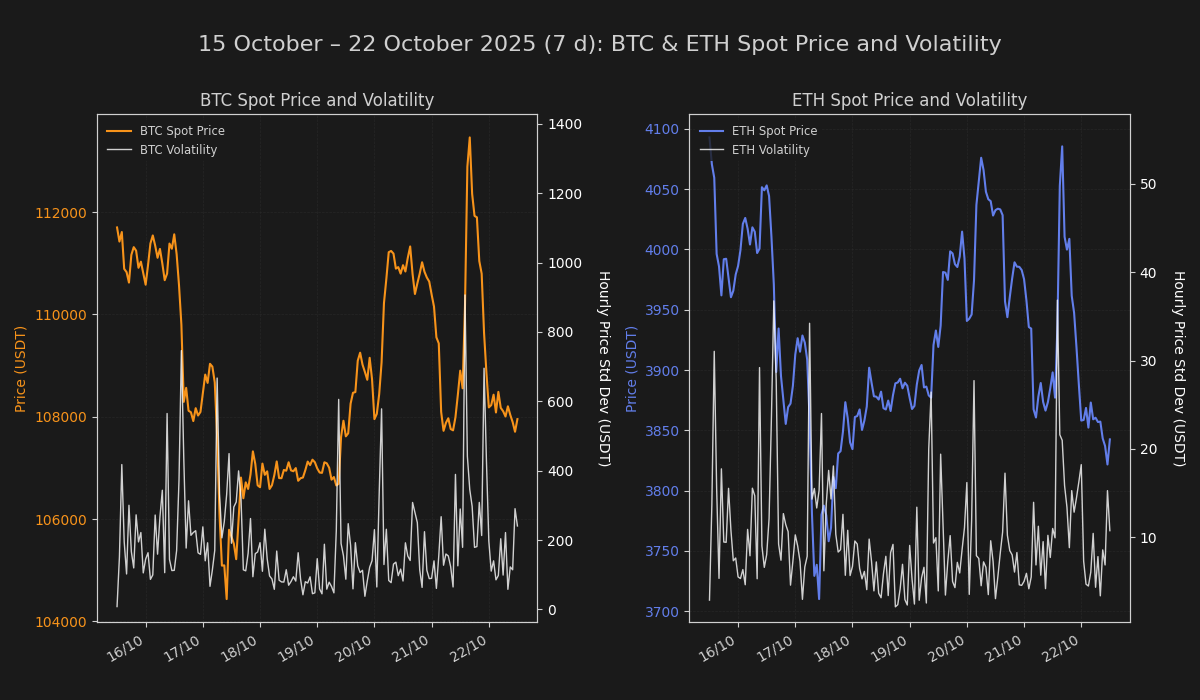

The weekly review of derivatives and rates activity confirms a significant de-risking cycle following a sharp price retracement in the underlying assets. Bitcoin's decisive slide from the $115,000 handle and subsequent bounce near $104,000 effectively purged speculative positioning. The market structure remains fragile, characterized by defensive rotation and a palpable shift from aggressive directional conviction to capital preservation.

Rates & Basis Analysis: Bitcoin and Ethereum

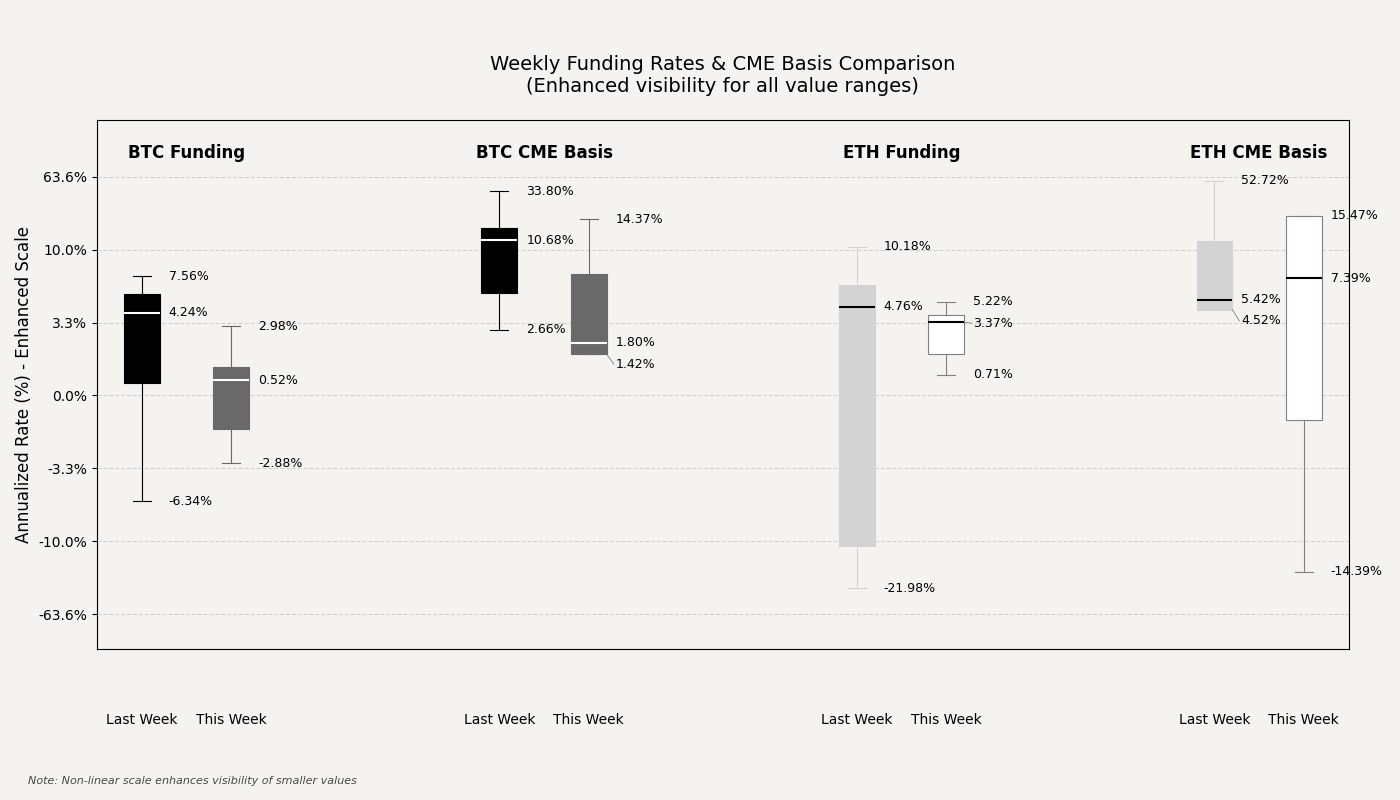

The derivatives landscape for the majors, Bitcoin BTC and Ethereum ETH exhibits a marked normalization from previously elevated levels. Centralized Exchange (CEX) perpetual funding rates for BTC experienced a profound collapse this week.

The daily annualized average plummeted to a near-zero or slightly negative territory, hovering around 0.05%, a stark divergence from the robust 4.50% average observed in the preceding period. This swift move, which included multiple days of negative prints, signals a powerful flush of the long base and a temporary switch to a net short bias among perpetual traders.

ETH funding rates echoed this sentiment, albeit with slightly less severity. The ETH daily annualized average converged to approximately 2.60% this week, down dramatically from a prior average of 7.60%. The volatility in ETH funding was particularly pronounced, with daily rates oscillating from extreme positivity to negative prints, indicating a highly contested and volatile liquidation process.

The forward term structure responded in a heterogeneous manner across regulated and offshore venues.

The CME Bitcoin basis saw a material deceleration in premium, with the daily annualized rate compressing sharply to an average of around 3.70% this week, down from the approximately 14.60% average in the previous period. This narrowing confirms a broader unwinding of the basis trade and reduced forward expectations in the regulated market. However, a significant dispersion in the daily data, including a deep negative reading, indicates bouts of illiquidity and sudden bearish hedging pressure within the contract.

The CME Ethereum basis also normalized from its prior volatility spike, with the weekly average settling at approximately 8.10% compared to the high-volatility, outlier-driven 15.10% average of the last period. Like BTC the daily ETH basis readings were highly volatile, including a notable instance of steep backwardation (negative basis), suggesting aggressive sell-side delta hedging was a key driver of regulated contract price action.

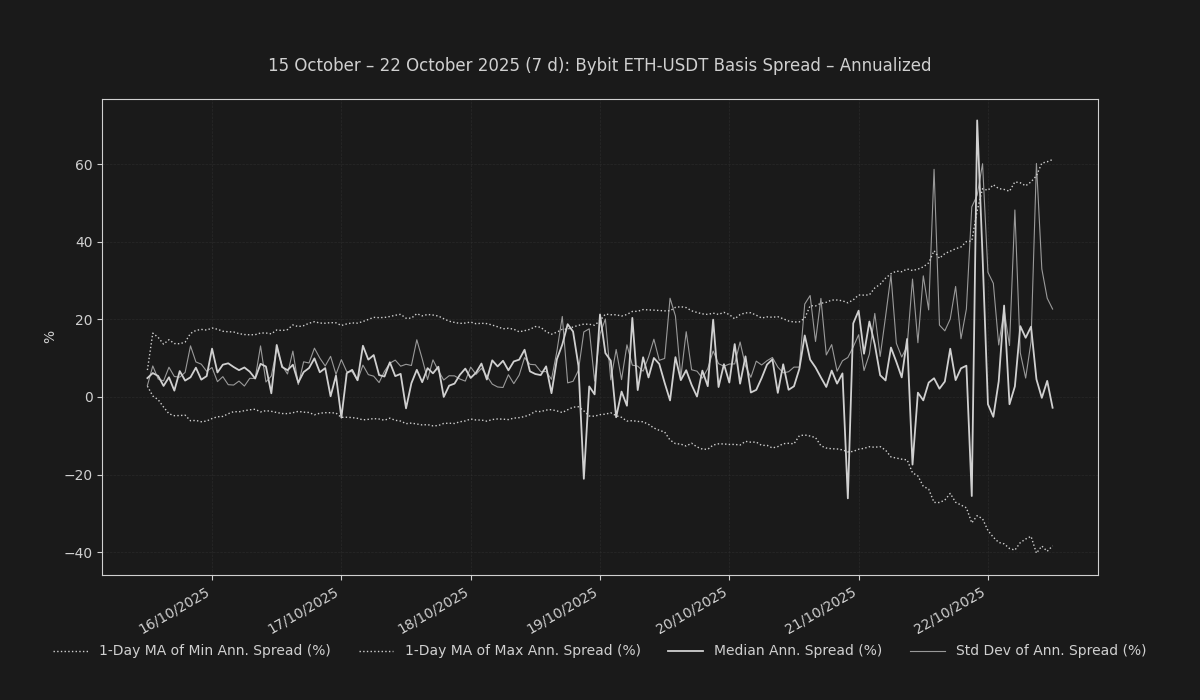

Looking at the offshore term structure on Bybit, the BTC quarterly futures basis (as a proxy for the three-month forward yield) closed the "Last 7 Days" period with a materially negative annualized premium of approximately -44.49%. This represents a dramatic shift from the preceding week and is highly indicative of strong counter-trend positioning or aggressive, structural hedging activity dominating the far-month contract. The ETH Bybit quarterly basis closed at an annualized -17.68%, similarly reflecting a substantial deterioration in forward market expectations and a move into backwardation.

Funding Arbitrage & Market Dislocations

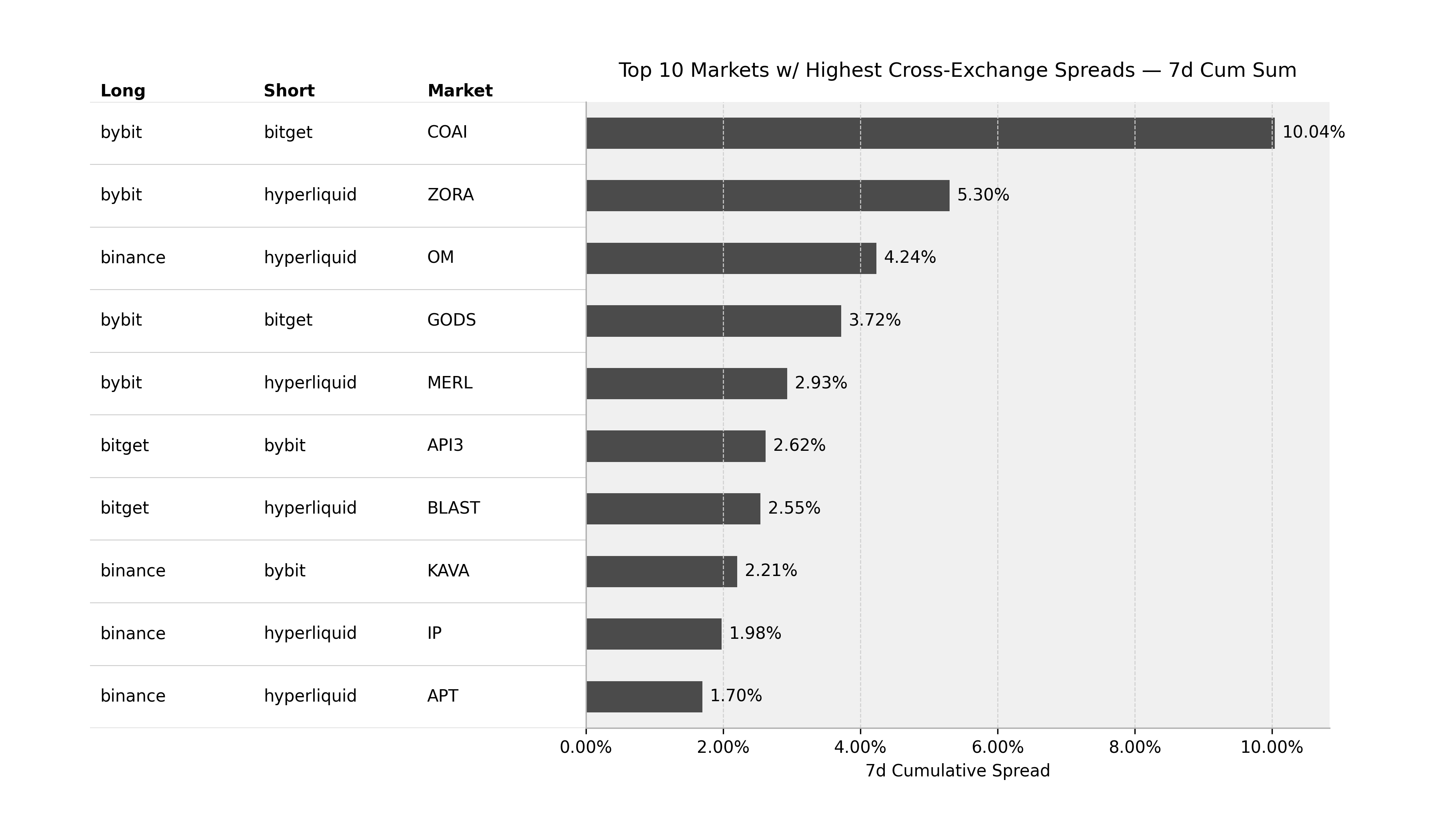

Despite the broad decline in perpetual funding levels, material cross-exchange rate dislocations continue to offer compelling high-probability arbitrage opportunities. The largest cumulative seven-day spread was identified in COAI, where a long position on Bybit financed by a short on Bitget generated a raw cumulative spread of 0.1004. A secondary significant opportunity was observed in the ZORA market, yielding a raw cumulative spread of 0.0530 for a long position on Bybit hedged by a short on Hyperliquid. These persistent spreads underscore a continued fragmentation in liquidity and idiosyncratic pricing across smaller-cap assets.

Altcoin Funding Dynamics

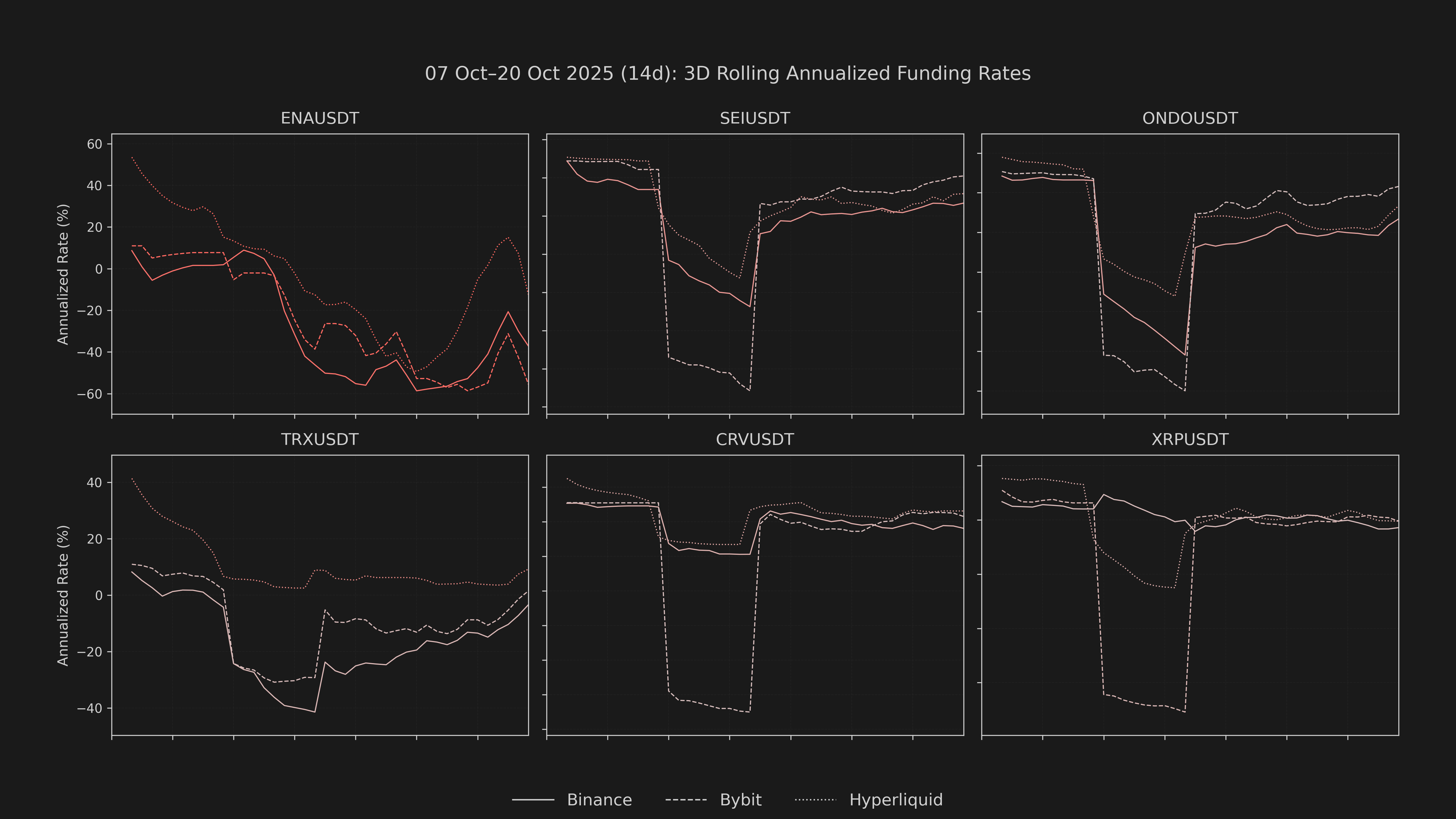

Altcoin funding activity suggests a highly heterogeneous yet structurally less leveraged environment. A key observation is the pronounced deterioration in the ENA funding rate. On Bybit, the ENA 8-hour cumulative funding rate for the week closed at a negative -0.001196, representing a substantial drop from the previous week's slightly positive close, indicating a significant influx of short interest or a liquidation-induced drop in long exposure. Conversely, SEI on Binance demonstrated a notable rebound, with its cumulative 8-hour funding rate shifting from a marginally negative close in the prior week to a positive 0.0001 this week, suggesting a localized, renewed push for long exposure or a reduction in short-side pressure.

Conclusion

The market's decisive deleveraging is unequivocally reflected in the sharp compression of CEX perpetual funding rates and the material narrowing and occasional backwardation of the futures basis across both regulated and offshore venues. The current rates environment significantly diminishes the appeal of the long-side carry trade and points to a period where dealer books are relatively cleaner but positioned defensively, awaiting a fundamental catalyst to re-engage directional risk.