.png)

.png)

Weekly Recap : Crypto Rates W49

Market Overview

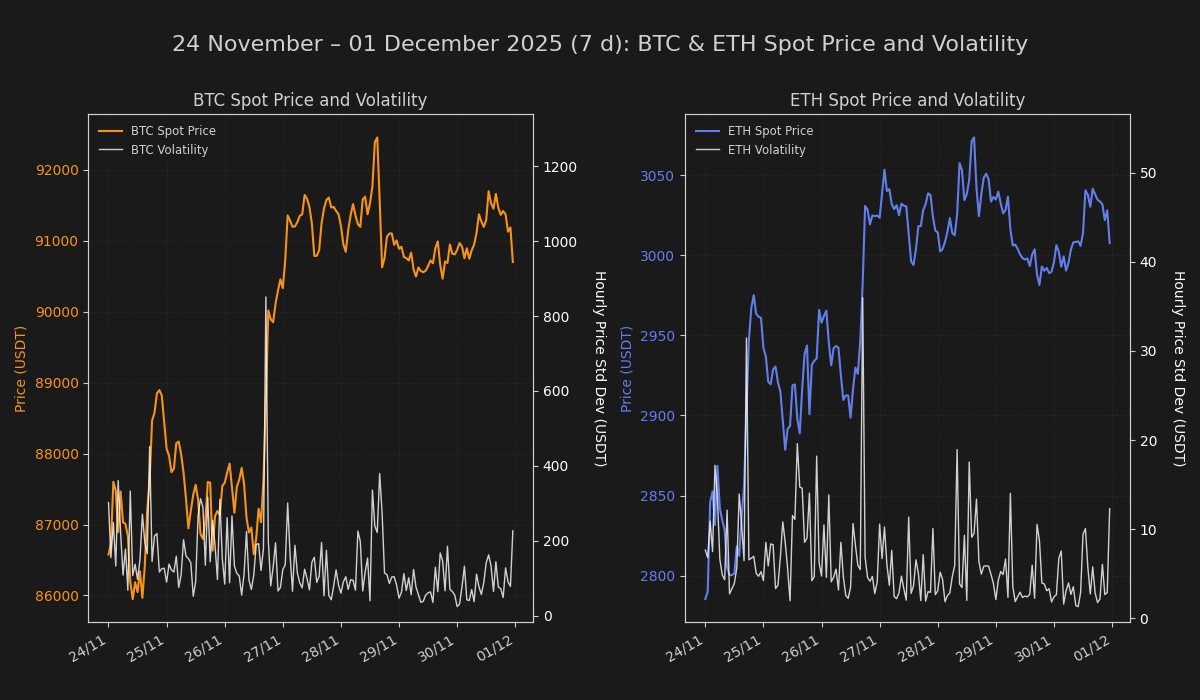

Bitcoin has stabilized above recent support zones following a measured deleveraging cycle, with price action consolidating in a range-bound pattern as participants reassess positioning. The broader complex is exhibiting signs of exhaustion following several weeks of downward pressure, though conviction remains tentative amid compressed volumes and cautious institutional flows.

Rates & Basis Analysis: Bitcoin and Ethereum

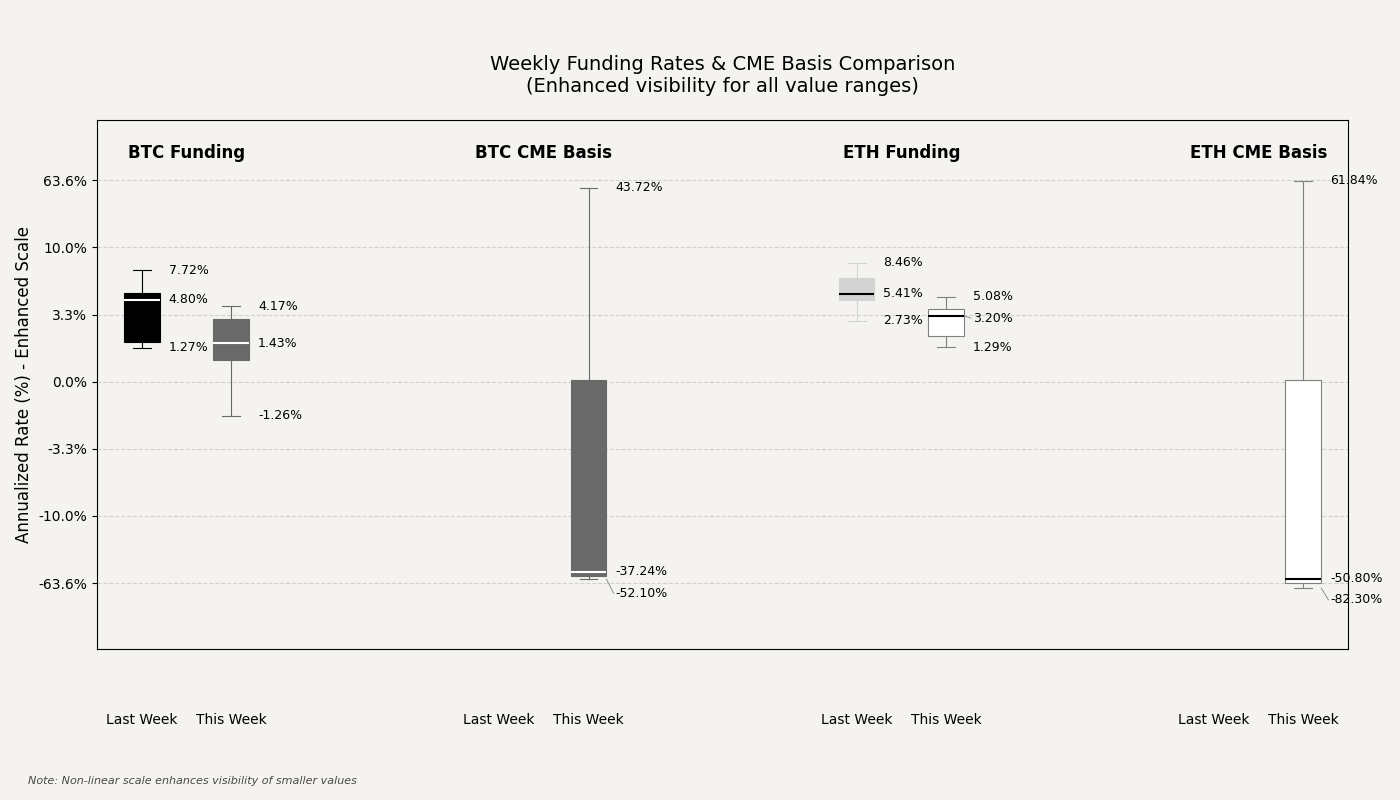

The most pronounced development in derivatives markets this period has been the dramatic rebalancing of perpetual swap funding costs, particularly for Bitcoin. Where the prior observation window saw annualized funding rates consistently anchored in the 5-10% zone, reflecting persistent willingness to pay for leverage, the current period marks a decisive inflection. Bitcoin funding rates experienced sharp mean reversion, with daily observations oscillating around the 1-2% level and briefly crossing into negative territory mid-period. This represents a collapse of approximately 500 basis points in average carry costs week-over-week, signaling an aggressive flush of speculative long positioning.

Ethereum's funding trajectory, while exhibiting similar directionality, has demonstrated notably greater resilience. Daily funding costs moderated from an average near 6.5% to approximately 3.3%, marking a compression of roughly 320 basis points. The differential in adjustment magnitude between BTC and ETH suggests that Ethereum's perpetual markets retained a stickier leverage profile, with longs less willing to capitulate despite the broader unwind. The closing prints for ETH funding this period settled near 5%, indicating a stabilization at levels still reflective of modest bullish sentiment.

The regulated futures market exhibited extraordinary turbulence, with the CME basis for both Bitcoin and Ethereum oscillating between extreme backwardation and steep contango throughout the observation period. Bitcoin's annualized basis recorded intraday prints ranging from approximately -52% to +44%, a volatility profile consistent with acute liquidity fragmentation and aggressive delta-hedging activity by authorized participants. Ethereum demonstrated an even wider amplitude, swinging from roughly -82% backwardation to +62% contango, suggesting heightened basis risk and potential inventory management pressures among institutional market-makers.

This erratic behavior in regulated term structure, particularly the episodes of severe backwardation, likely reflects transient dislocations driven by ETF creation/redemption mechanics rather than a fundamental bearish consensus. The normalization toward positive carry by period-end—with BTC settling near +44% and ETH near +62%—indicates these were execution-driven anomalies rather than sustained structural shifts. However, the magnitude of intraday basis swings underscores meaningful fragmentation between onshore and offshore liquidity pools.

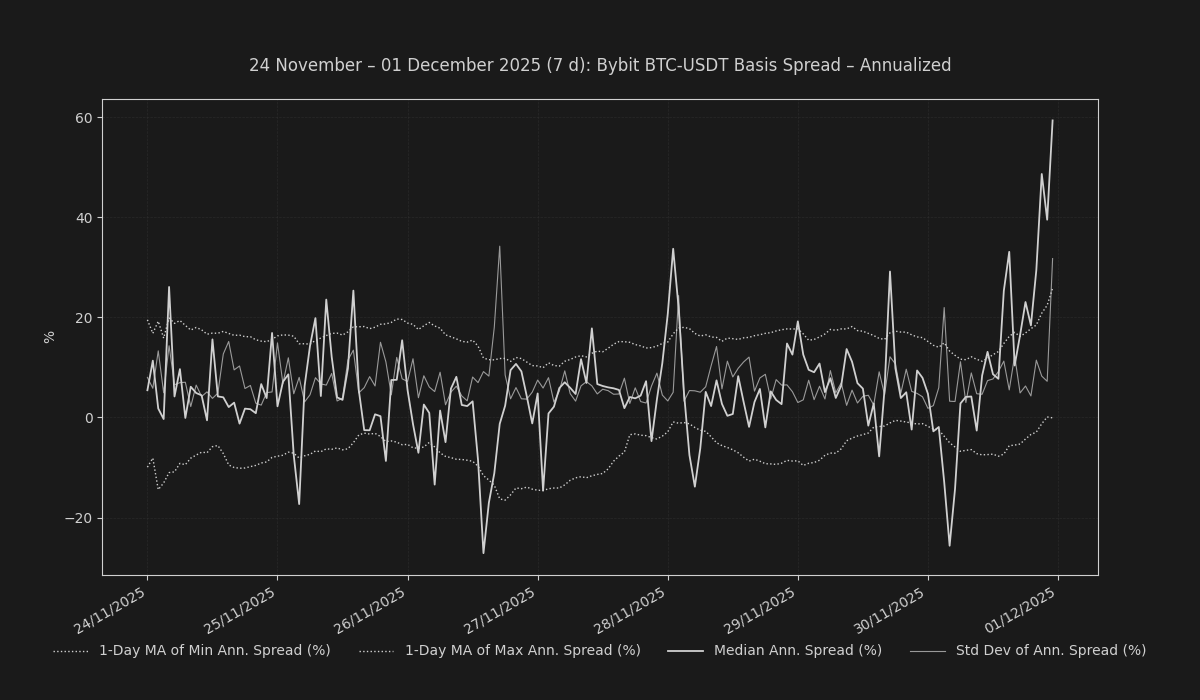

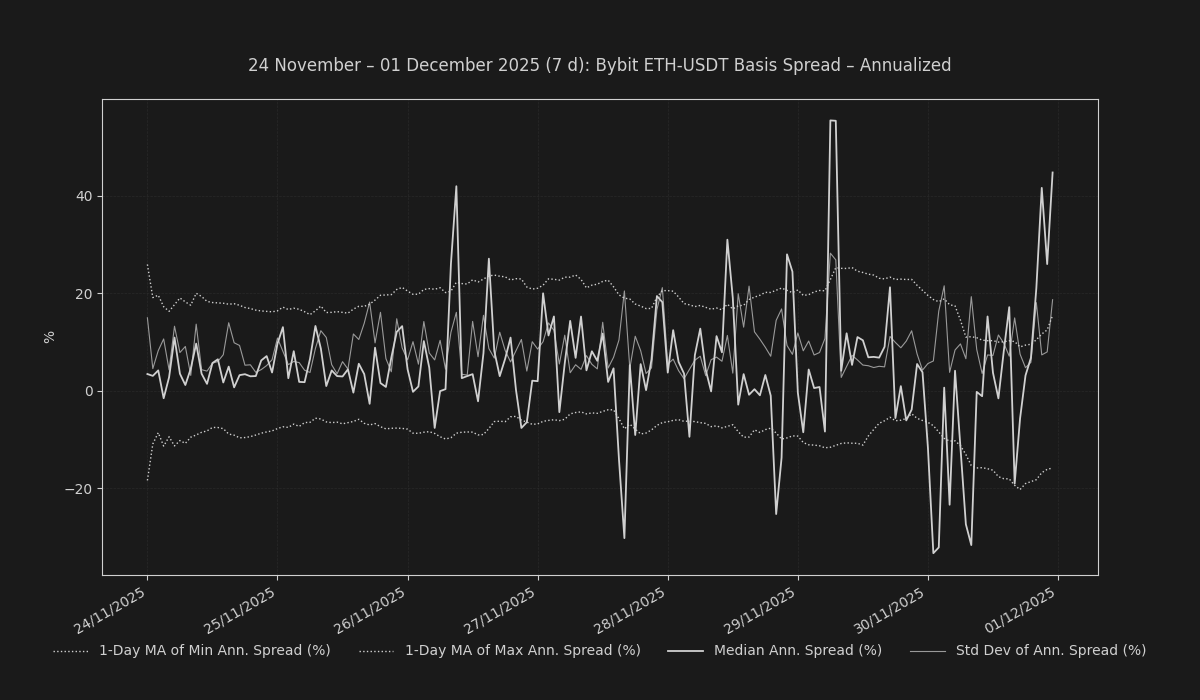

In contrast to both the perpetual funding compression and the CME volatility, the dated futures curve on Bybit continues to exhibit robust contango. Bitcoin's annualized basis closed the period at approximately 39%, while Ethereum settled even steeper at 45%. These elevated term structures, persisting despite the deflation in perpetual funding and the chaos in regulated futures, suggest a bifurcation in market structure: near-dated leverage has been aggressively unwound, yet participants remain willing to pay significant premiums for exposure via quarterly contracts.

This divergence may reflect either expectations of renewed volatility expansion or positioning by market-neutral desks seeking to harvest roll yield in anticipation of futures convergence as expiry approaches.

Funding Arbitrage & Market Dislocations

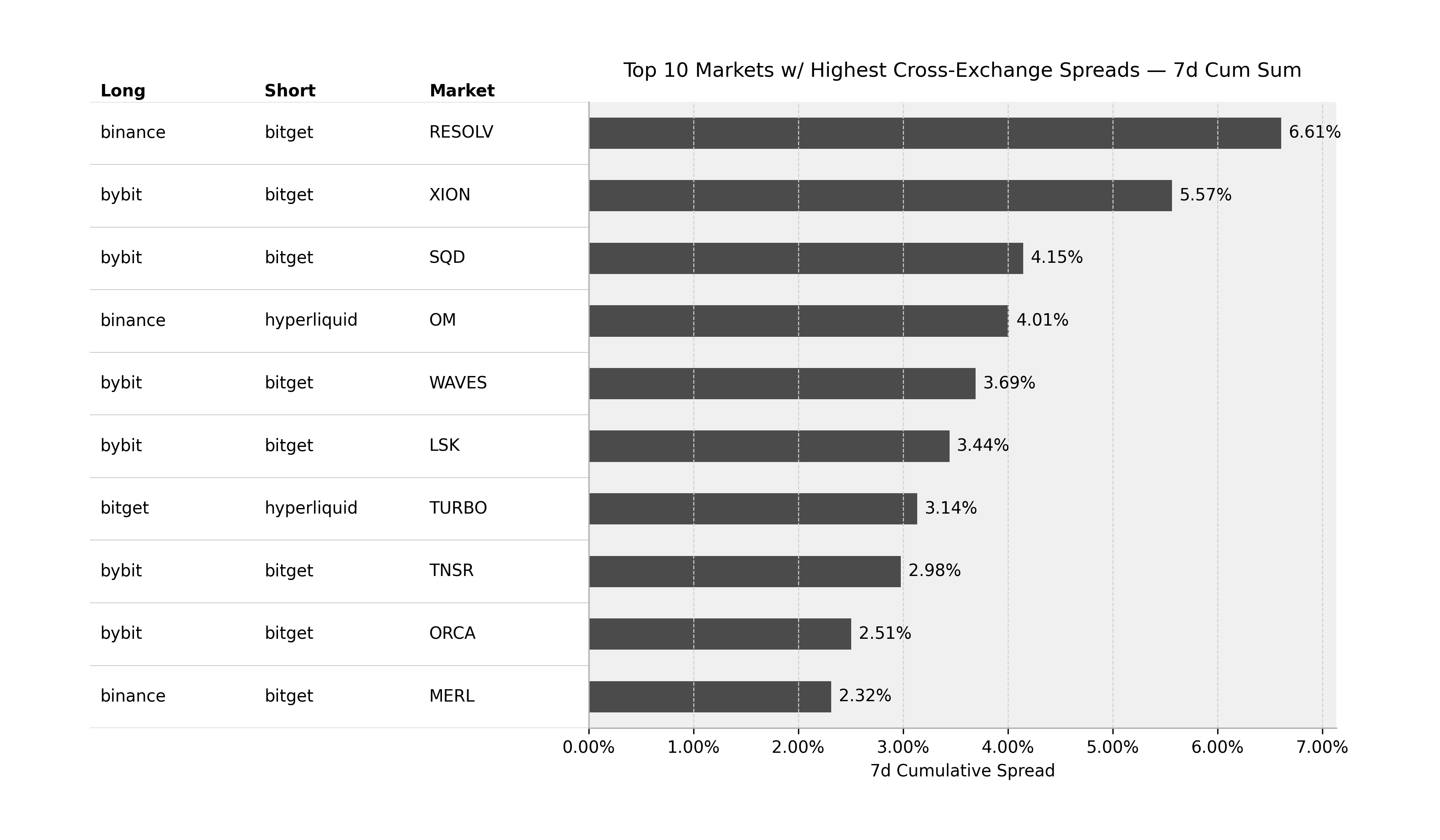

Fragmentation across exchange venues has intensified, creating compelling opportunities for capital-efficient arbitrage strategies. The most substantial venue dislocation emerged in RESOLV, where a persistent imbalance generated a cumulative raw spread of approximately 6.6% over the seven-day measurement window by simultaneously holding long exposure on Binance and short on Bitget.

This disparity was driven by Binance exhibiting sustained negative funding while Bitget maintained near-neutral rates, likely attributable to differing liquidity profiles and participant composition across the two venues.Similarly, XION presented an attractive spread of 5.6%, captured through a long Bybit / short Bitget structure.

The prevalence of Bitget as the short leg across multiple top-tier opportunities suggests systematic underpricing of carry on that venue relative to peers, potentially reflecting differences in market-making incentives or directional flow skew. Additional meaningful spreads materialized in SQD (4.1%) and OM (4.0%), with the latter involving Hyperliquid as the short venue, highlighting the platform's increasing integration into cross-exchange arbitrage flows.

Altcoin Funding Dynamics

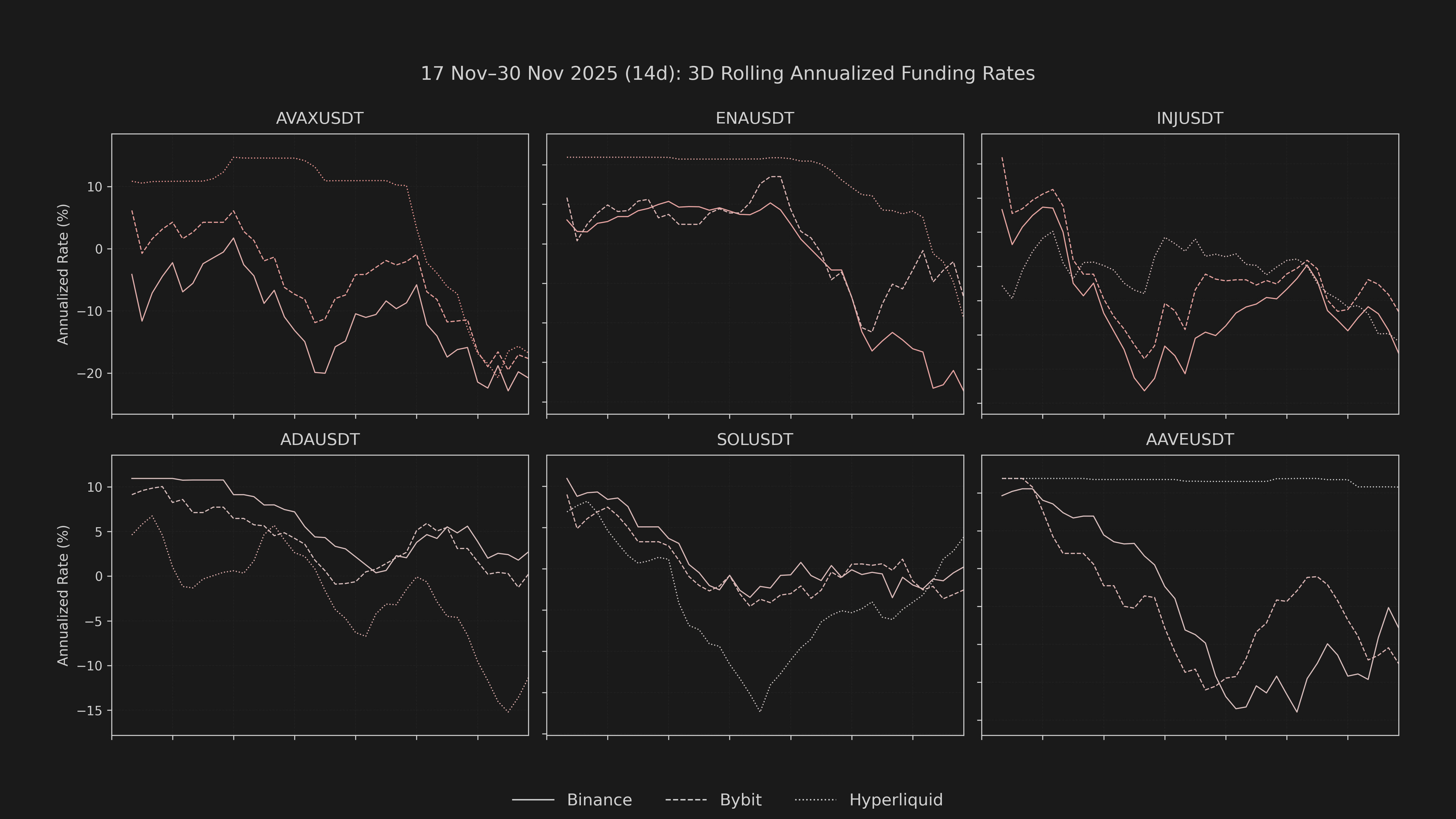

Beneath the major assets, select altcoins experienced pronounced sentiment reversals, as evidenced by dramatic funding rate dislocations. Ethena (ENA) exhibited the most severe deterioration, with 8-hour funding sums on Binance collapsing from modestly positive territory (+0.000019) in the prior period to deeply negative (-0.000405) this week.

This approximately 2000% shift represents a complete capitulation of bullish positioning, with participants now actively paying to maintain short exposure. Bybit mirrored this breakdown, with ENA funding plunging from near-neutral to -0.000312, confirming a broad-based reassessment of the asset's near-term prospects across venues.

Conversely, HYPE demonstrated a remarkable recovery in sentiment. On Bybit, the token's funding profile reversed from negative (-0.000084 previously) to the maximum positive rate (0.00010), indicating a surge in speculative demand and willingness to pay for long exposure.

This 220% swing positions HYPE as an outlier in the current environment, where most assets are experiencing funding compression or deterioration.Injective (INJ) continued its descent into negative carry territory, with Binance funding declining from -0.000116 to -0.000275, while Bybit similarly weakened from -0.000125 to -0.000219. The persistent bearish skew across multiple venues suggests sustained structural selling pressure rather than transient dislocation.

Conclusion

The present configuration reflects a market in transition: aggressive deleveraging in perpetual swaps has driven funding rates toward neutral, while the CME basis volatility signals acute stress in institutional hedging flows, likely tied to ETF mechanics. The normalization of onshore basis back into contango by period-end, coupled with persistently elevated offshore term structure, suggests the worst of the dislocation may be resolving. For relative value allocators, the current environment offers rich cross-venue yield opportunities, particularly in altcoin markets where sentiment fragmentation has widened spreads to multi-month extremes. Directional conviction, however, remains absent, as evidenced by the collapse in carry costs and the persistence of low-volume consolidation.