.png)

.png)

Weekly Recap : Crypto Rates W36

Market Overview

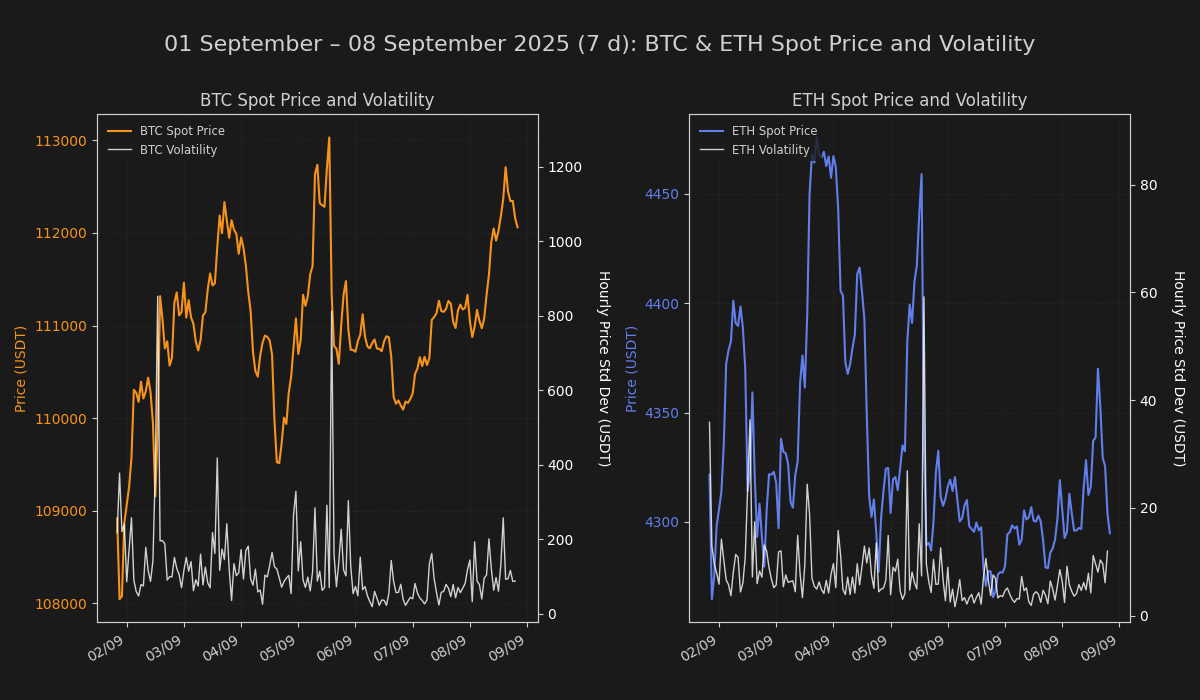

The digital asset market found a fragile equilibrium this week, with prices stabilizing after recent volatility. However, the recovery lacked conviction, as evidenced by declining trading volumes and defensive posturing in derivatives markets, suggesting participants remain cautious and are awaiting a more definitive catalyst.

Rates & Basis Analysis: Bitcoin and Ethereum

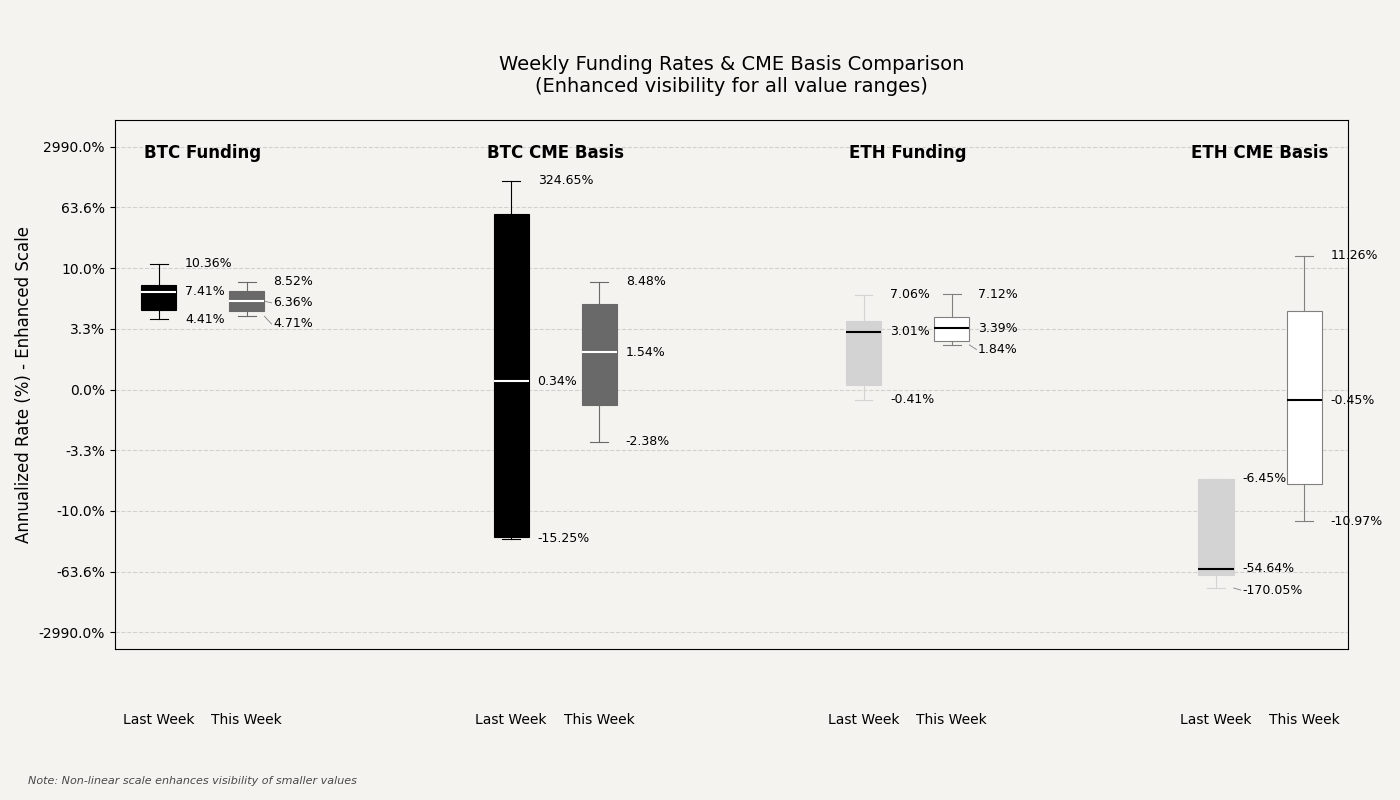

The cost of carry in perpetual futures markets saw a general easing this period. Bitcoin's annualized funding rates compressed slightly, averaging around 6.4%, down from approximately 7.0% in the preceding week, reflecting a more balanced sentiment between long and short speculators. Ethereum funding rates remained subdued, ticking up modestly to a 3.1% average but still indicative of a market lacking aggressive directional appetite.

A significant development occurred in the CME term structure, which underwent a dramatic normalization. After a period of extreme dislocation, both Bitcoin and Ethereum futures bases saw their volatility collapse, with spreads narrowing significantly to trade in a tight range around par. This suggests that the acute institutional hedging pressures observed previously have subsided, allowing the basis to return to a more stable equilibrium.

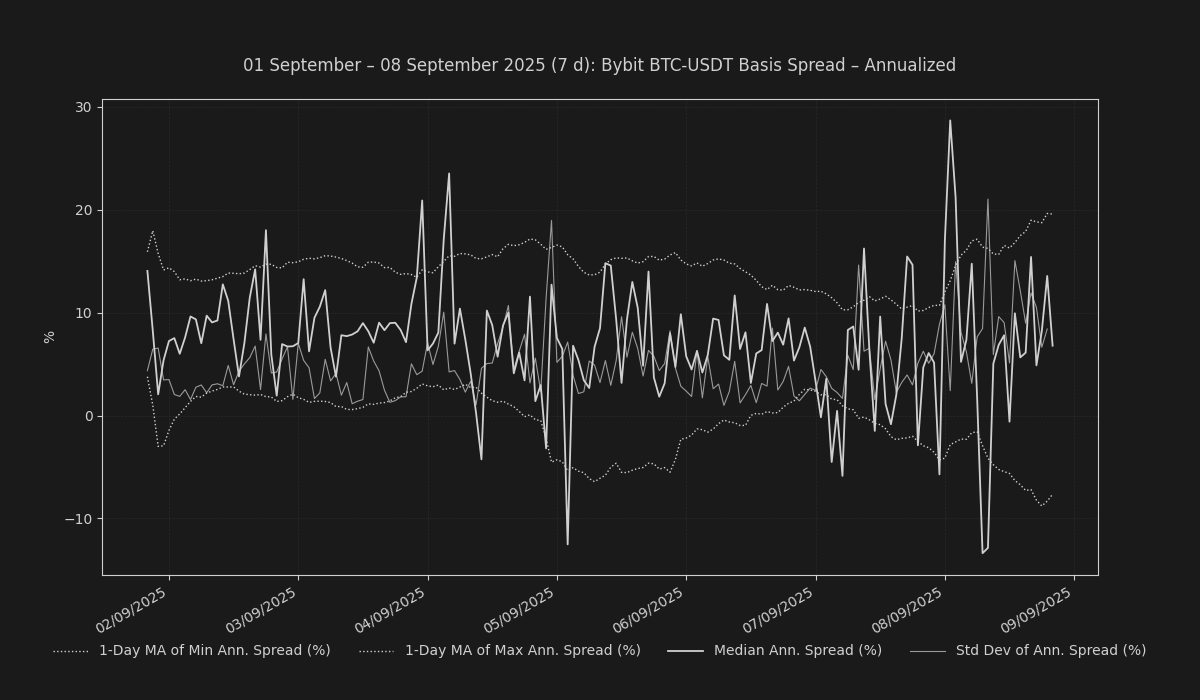

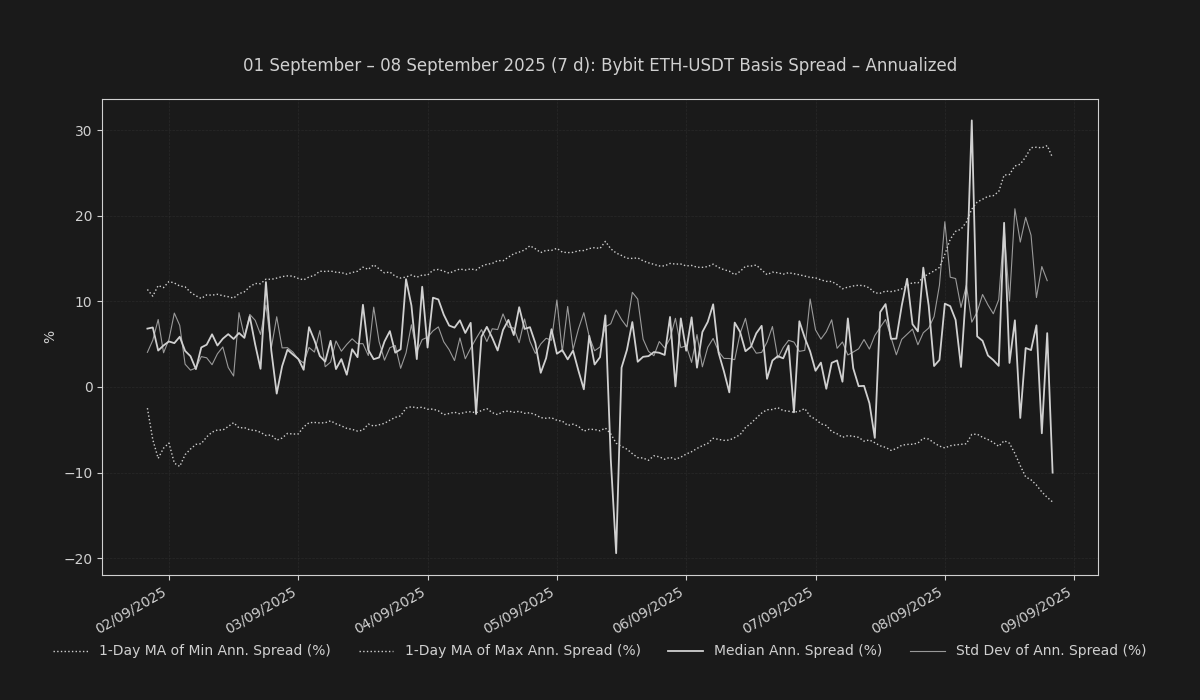

This trend of basis compression was also evident in offshore venues. The annualized basis for Bitcoin on Bybit tightened considerably, closing the week near 6.8%. More notably, Ethereum’s term structure flipped into backwardation, settling at a discount of approximately -10.0%, signaling weakening demand for forward-dated ETH exposure.

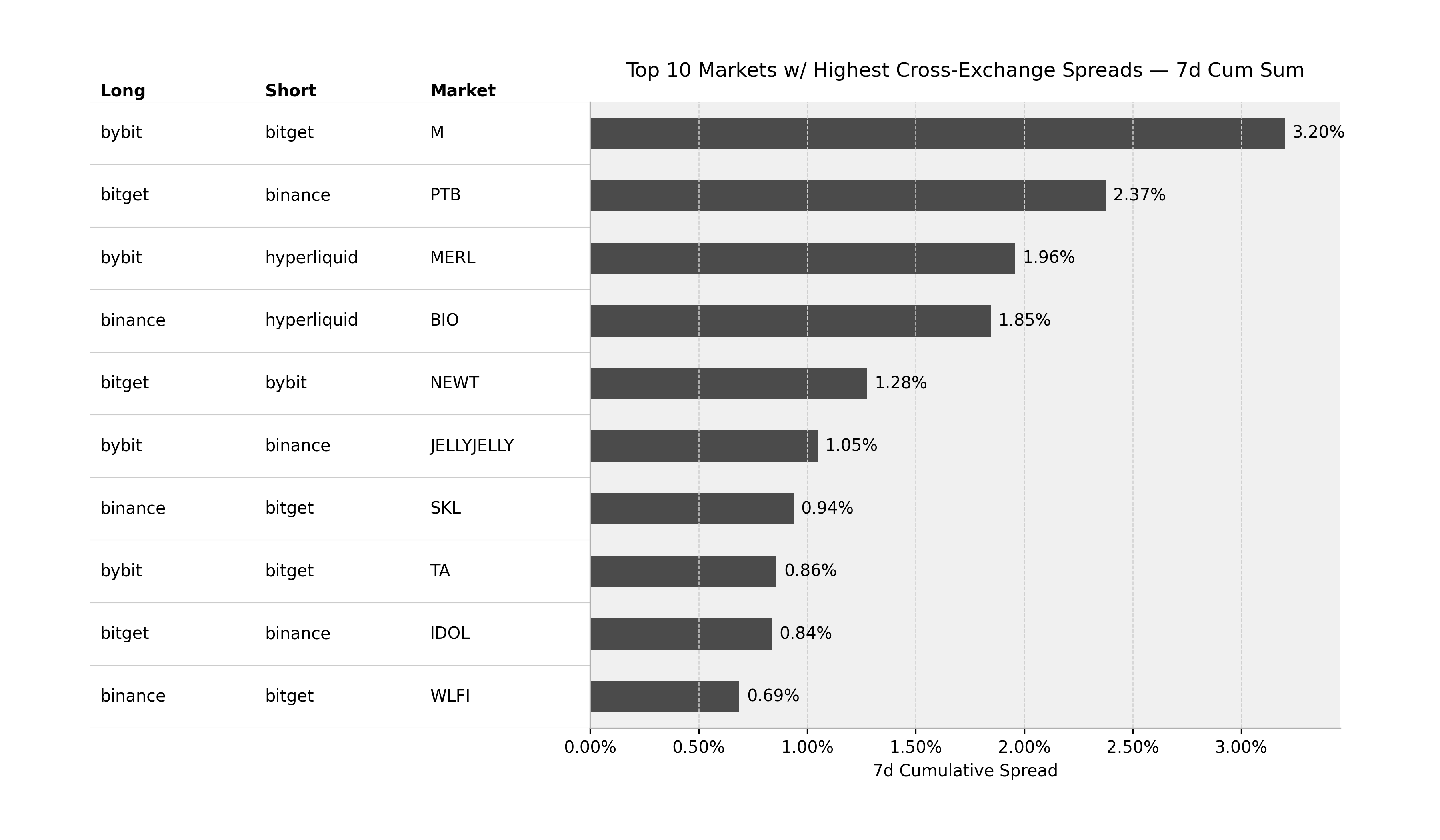

Funding Arbitrage & Market Dislocations

Structural inefficiencies between trading venues continued to offer attractive arbitrage opportunities. The most significant dislocation was present in the M market, where a strategy pairing a short on Bitget with a long on Bybit would have captured a cumulative spread of roughly 3.20% over seven days. Another compelling trade was in PTB, with a short Binance against a long Bitget position yielding a cumulative 2.37%, underscoring persistent fragmentation in altcoin liquidity.

Altcoin Funding Dynamics

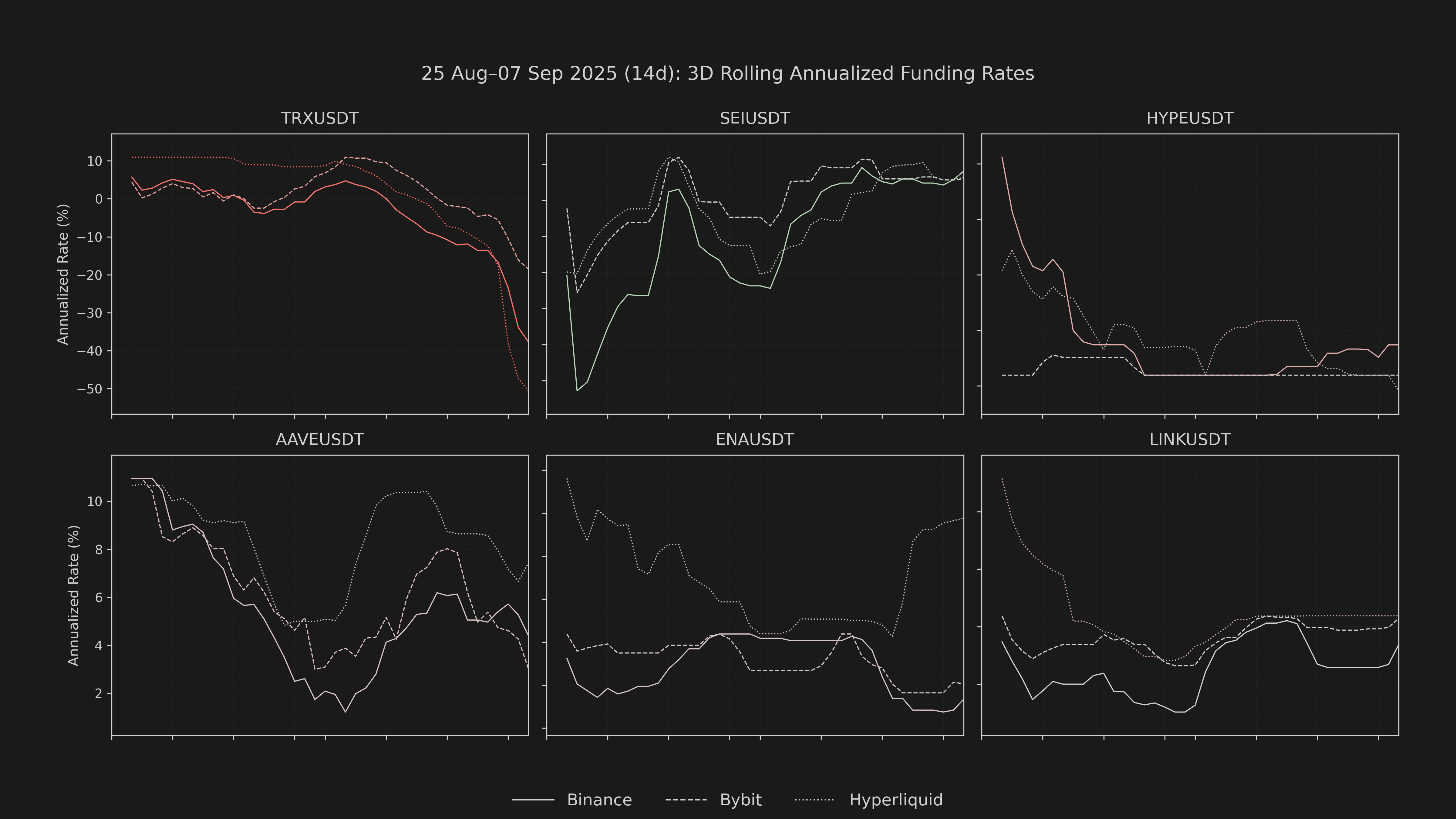

Sentiment shifts within the altcoin complex were highly idiosyncratic. Funding for TRX on Binance, for instance, flipped decisively negative, with its cumulative rate moving from positive territory in the prior week to a deep discount. This points to a significant build-up of short-side interest. In contrast, INJ on the same exchange saw its funding rate revert from negative to positive, suggesting a potential exhaustion of selling pressure and a renewal of speculative long interest.

Conclusion

The rates landscape reflects a market transitioning from a state of high volatility to one of cautious stability. The pronounced calming of the CME basis and the general compression across funding and term futures indicate a significant reduction in systemic stress. However, the lack of a strong positive carry suggests that conviction remains low, positioning the market in a holding pattern as it awaits a new directional narrative.