.png)

.png)

Weekly Recap : Crypto Rates W29

Market Overview

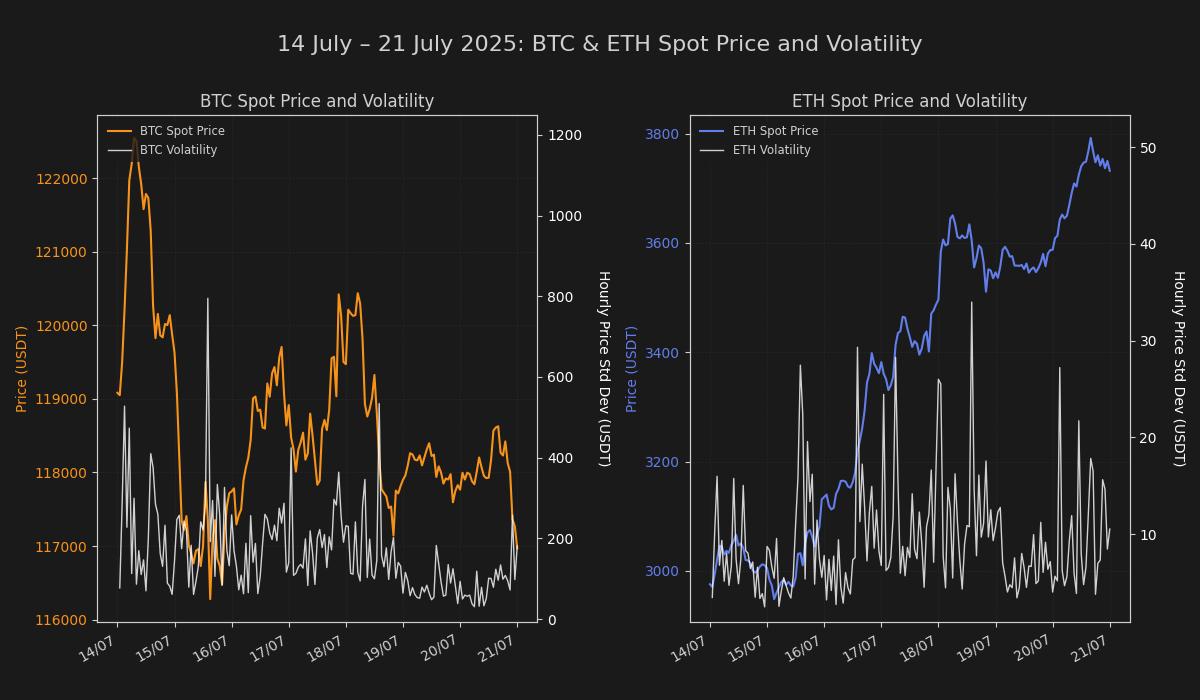

Digital asset markets entered a consolidation phase after a period of strong upward momentum, with directional conviction waning as prices retreated from recent highs. The current price action reflects a market absorbing prior gains, characterized by emergent profit-taking from short-term participants, even as underlying demand fundamentals appear to hold resilient.

Rates & Basis Analysis: Bitcoin and Ethereum

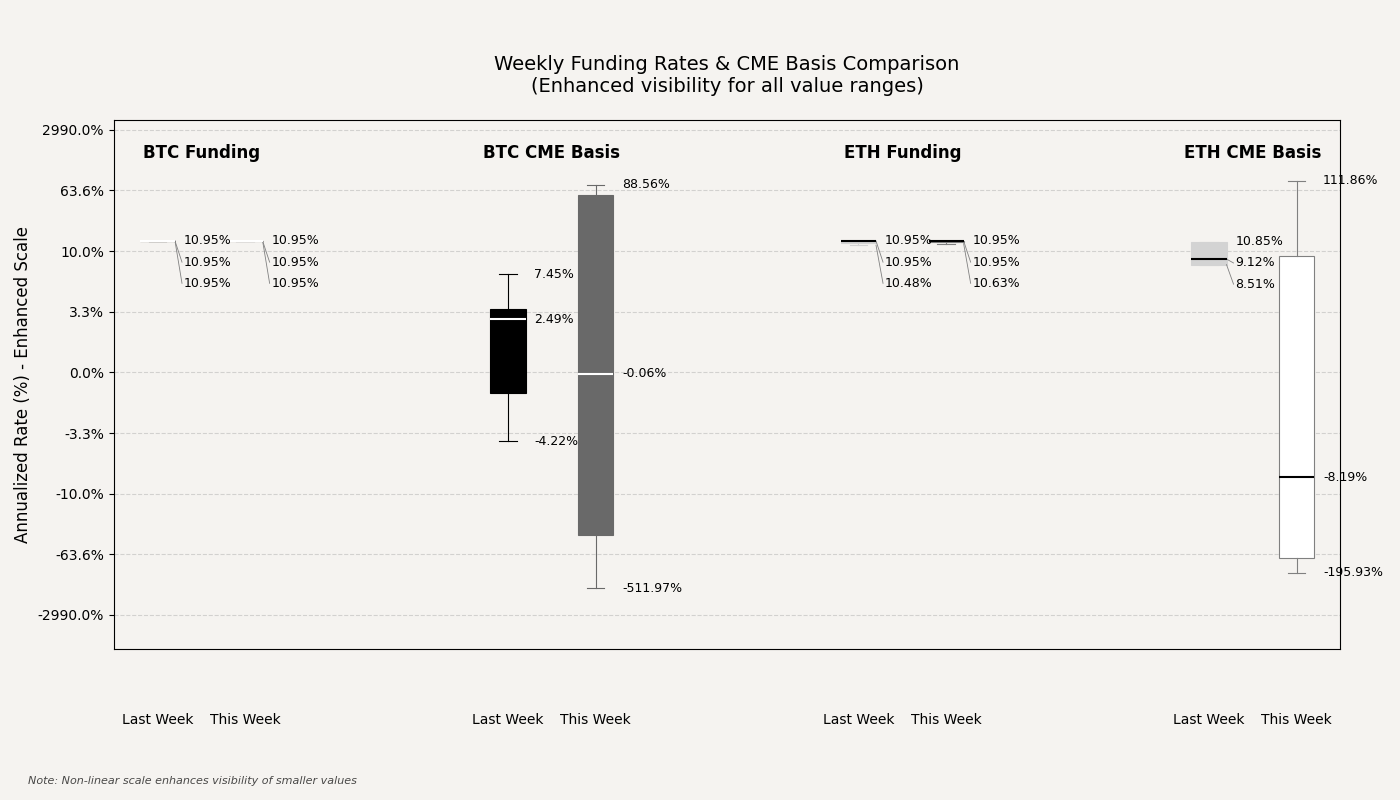

The cost of leverage in perpetual swaps remained structurally firm, signaling persistent demand for long-side exposure. Bitcoin’s annualized funding rates held near 11%, a slight elevation from the prior week's average around 10%, indicating that speculative appetite has not materially reset despite the sideways price action. Ethereum funding rates exhibited a more pronounced increase, converging with Bitcoin's near 11% from a lower base of approximately 9.3% in the preceding period. This convergence suggests a broadening of speculative interest into ETH, closing the relative valuation gap in leverage costs.

In stark contrast, the regulated futures market experienced a period of extreme dislocation. The CME basis for both Bitcoin and Ethereum exhibited unprecedented volatility, swinging from deeply negative to strongly positive territory. This severe term structure volatility points to significant, episodic hedging and arbitrage flows, likely from institutional participants repositioning amidst macroeconomic uncertainty and volatile spot markets. Such erratic basis behavior suggests a temporary breakdown in the pricing efficiency of institutional-grade instruments.

Offshore, the annualized basis on Bybit futures saw a notable compression. Bitcoin’s closing basis tightened dramatically to approximately 1.4% from over 13% in the prior seven-day period. Similarly, Ethereum's basis compressed to roughly 8.4% from 12.6%. This narrowing of the contango, coupled with a near-doubling of the standard deviation in basis for both assets, indicates heightened intraday volatility and a less certain directional view from offshore derivatives traders, contrasting sharply with the stable, high funding rates.

Funding Arbitrage & Market Dislocations

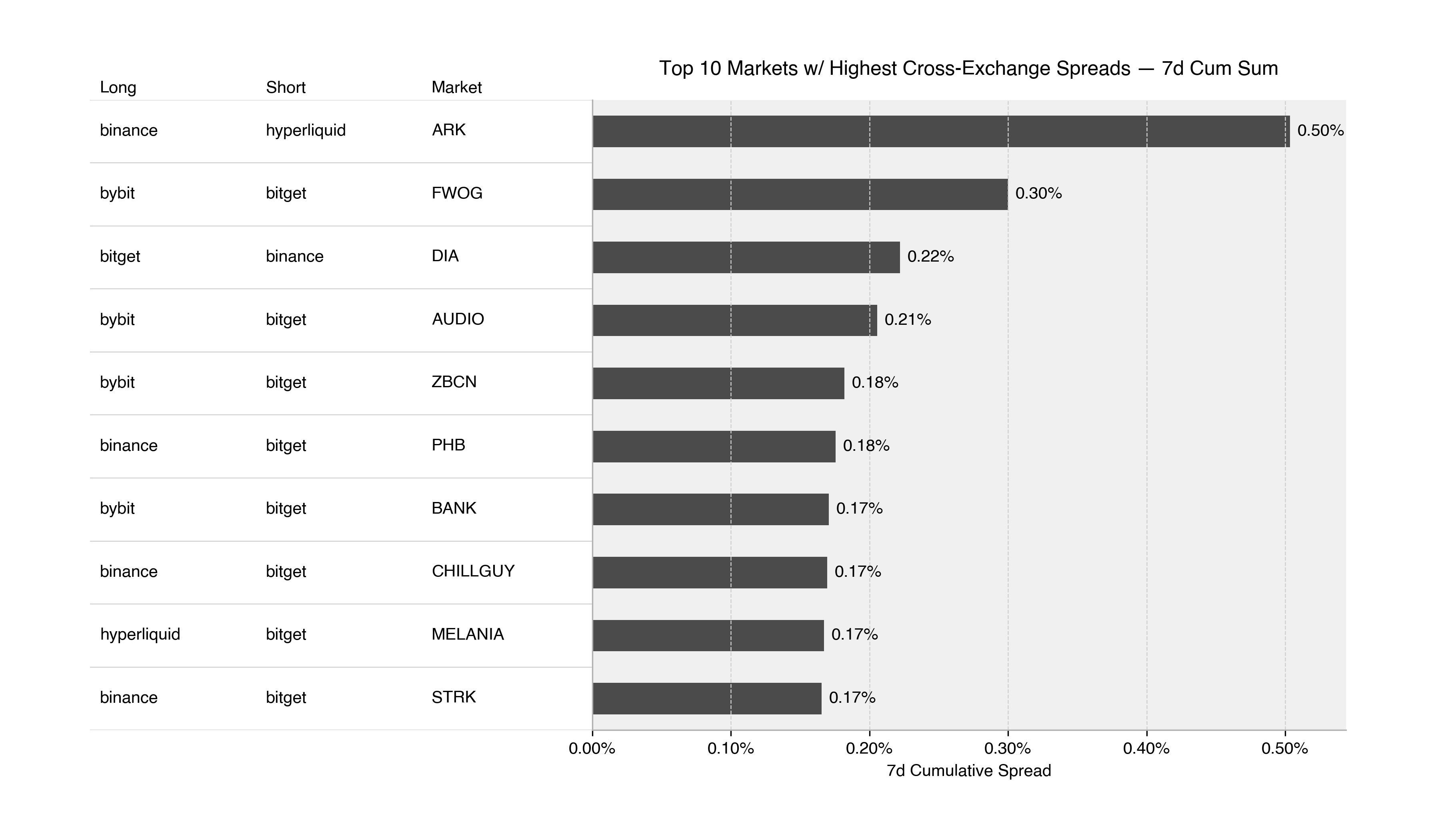

Cross-venue funding rate differentials exhibited marked compression this period, with maximum exploitable spreads contracting substantially from prior observations. The most attractive opportunity materialized in ARK perpetuals, offering a 50 basis point cumulative spread via long Binance/short Hyperliquid positioning, while FWOG presented a secondary 30 basis point dislocation through Bybit-Bitget pair trades. This narrowing of inter-exchange rate differentials suggests either enhanced capital efficiency in arbitrage deployment or reduced speculative intensity across venue-specific participant bases, indicating improved market microstructure integration relative to previous periods of acute fragmentation.

Altcoin Funding Dynamics

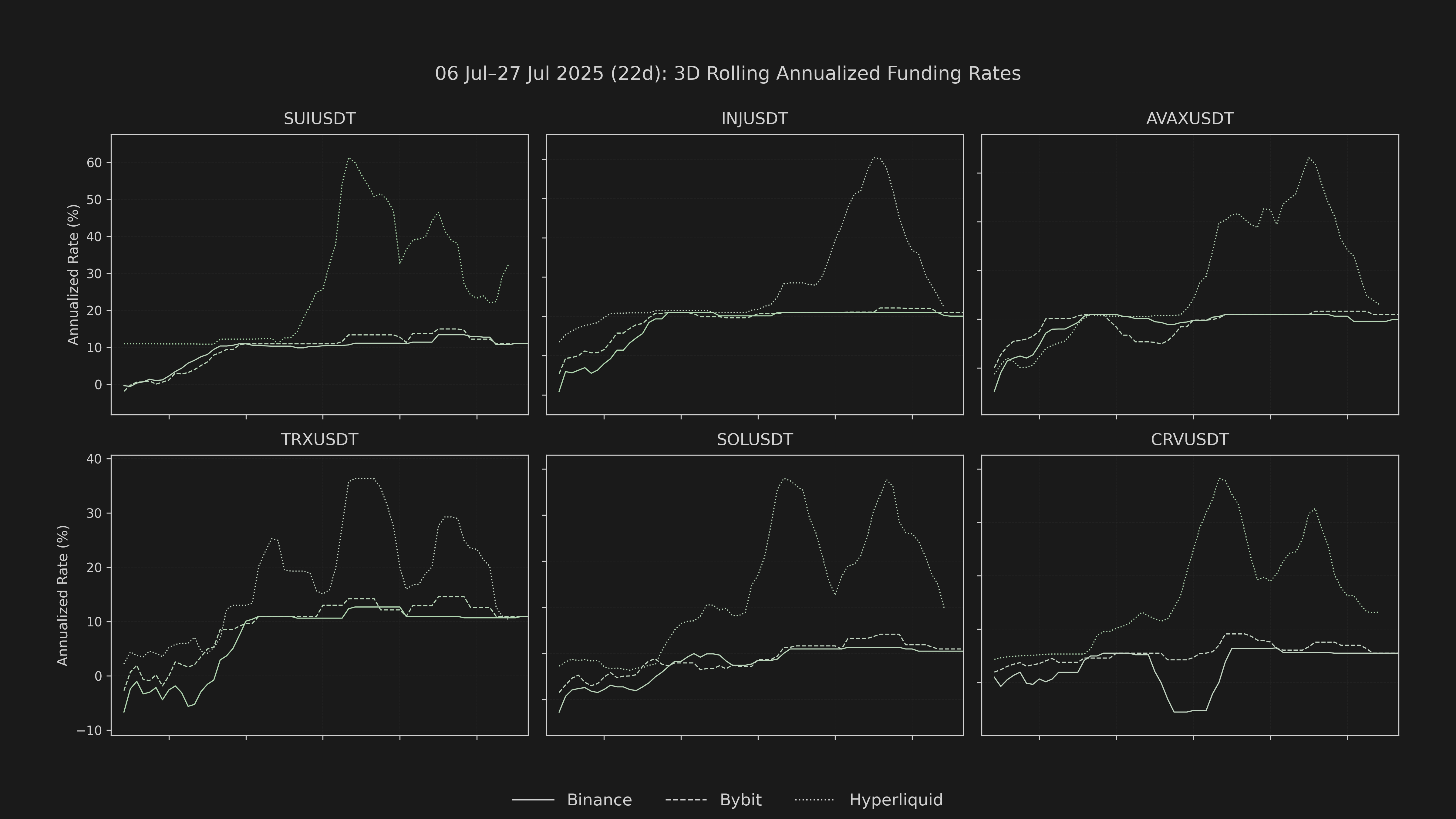

Selective positioning emerged within the altcoin complex, with funding rate dislocations concentrated in a handful of assets. SUI exemplified this dynamic, with Bitget rates surging to 35.4% annualized—a 24.5 percentage point expansion from the prior period—reflecting acute speculative demand amid otherwise subdued broader altcoin appetite. These concentrated flows underscore a tactical, theme-driven approach to risk-taking.

Conclusion

The prevailing rates architecture reveals a market characterized by structural tensions: persistent leverage demand coexists with acute term structure volatility in regulated instruments and compressing offshore basis spreads, indicating that systematic risk capacity remains constrained and vulnerable to rapid deleveraging events.