.png)

.png)

Weekly Recap : Crypto Rates W31

Market Overview

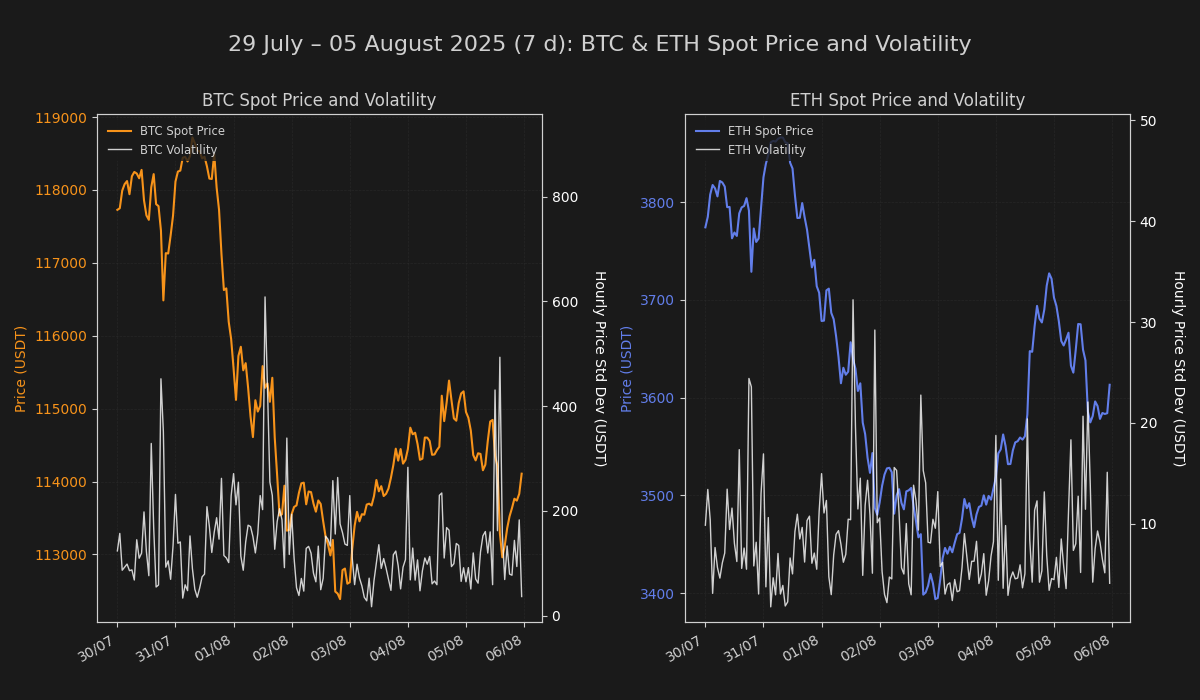

Digital asset markets experienced a period of price recalibration this week, with Bitcoin's momentum cooling significantly after its recent rally stalled below the $114k level. The broader market environment was characterized by a moderation in risk appetite, a decline in liquidity, and a noticeable shift towards cautious positioning as market participants reassessed their outlook.

Rates & Basis Analysis: Bitcoin and Ethereum

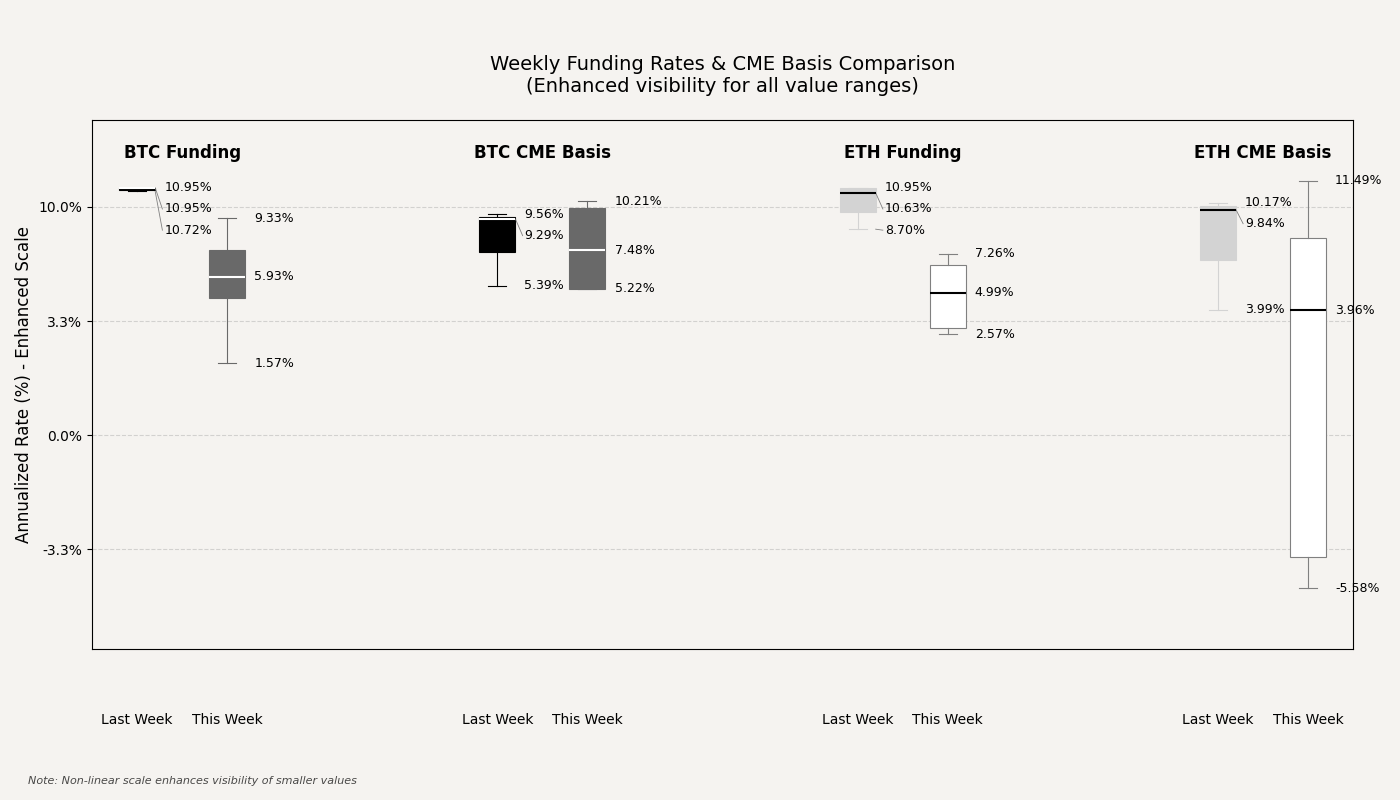

The cost of leverage in the perpetual futures market underwent a pronounced compression, reflecting a broad-based cooling of speculative demand. The annualized funding rate for Bitcoin, which was consistently elevated at approximately 10.95% in the prior period, saw a sharp decline this week, with daily values averaging around 6.5%. Similarly, Ethereum's funding rate experienced a more dramatic retreat, with the average falling from a robust 10.88% last week to a much lower average of around 5.0% this week. This collapse in funding costs underscores a significant deleveraging event among perpetual traders and a temporary abatement of the strong long-side positioning that had defined the prior period.

The CME futures basis for both Bitcoin and Ethereum exhibited extreme volatility and a major directional shift. For Bitcoin, the average daily basis inverted sharply from a positive 9.29% last week to a negative 1.5% this week, a move into deep backwardation. Ethereum's basis followed a similar, albeit more severe, trajectory, collapsing from a positive average of 10.17% to a negative 2.0% this week. This dramatic move points to a significant repositioning of institutional players within the regulated term structure, likely driven by a combination of hedging activity and risk-off sentiment.

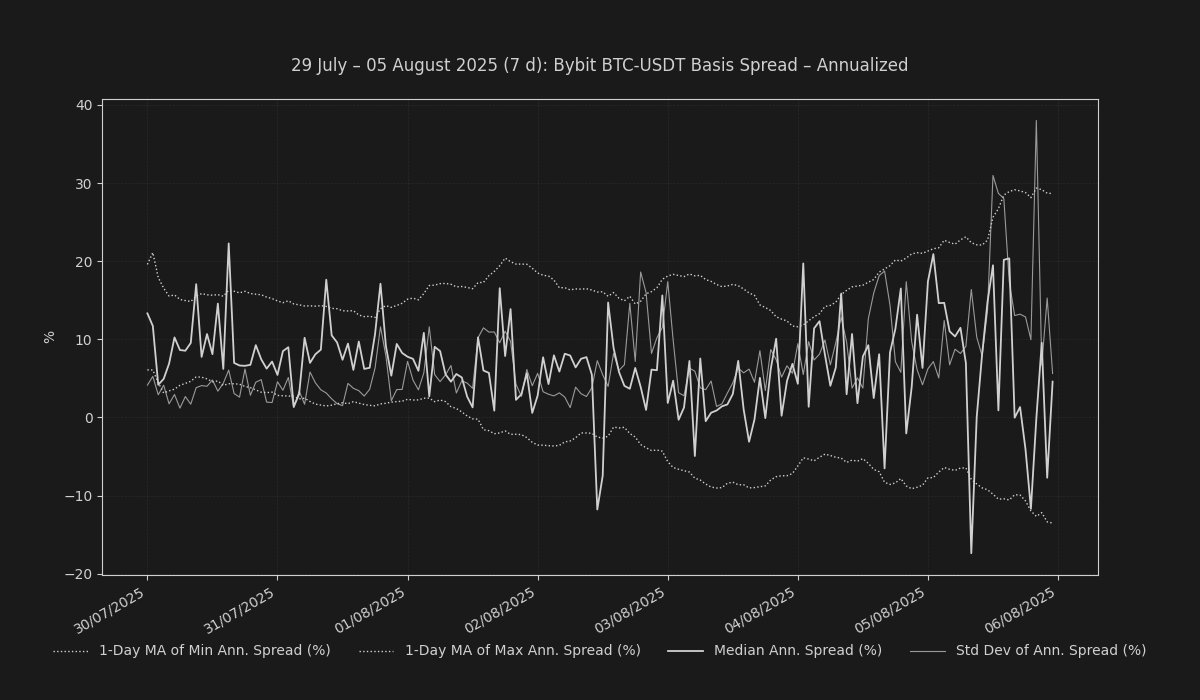

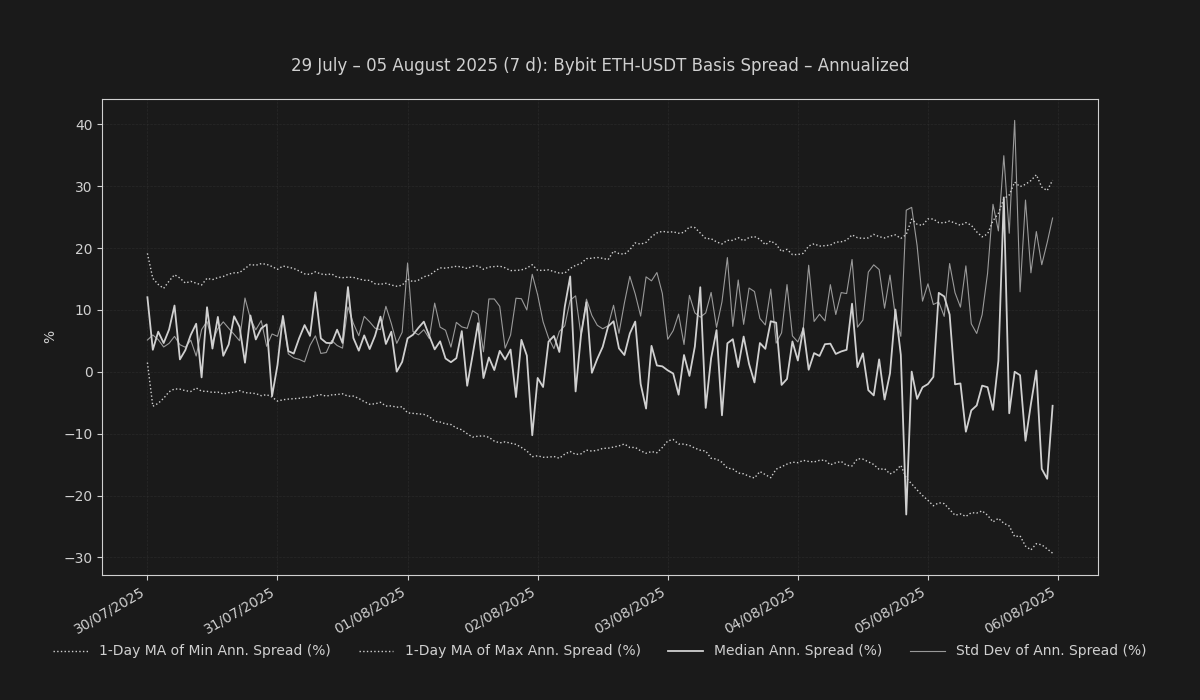

The offshore CEX (Bybit) futures basis for Bitcoin closed the week at a narrow 4.28%, a stark contraction from the prior period's robust spread. In contrast, the Ethereum basis on the same venue closed at a deeply negative -7.44%, indicating a sustained and acute backwardation. The persistent divergence between Bitcoin and Ethereum across both funding rates and basis signals a market that is pricing in distinct near-term risks for the two major assets, with a clear preference for Bitcoin.

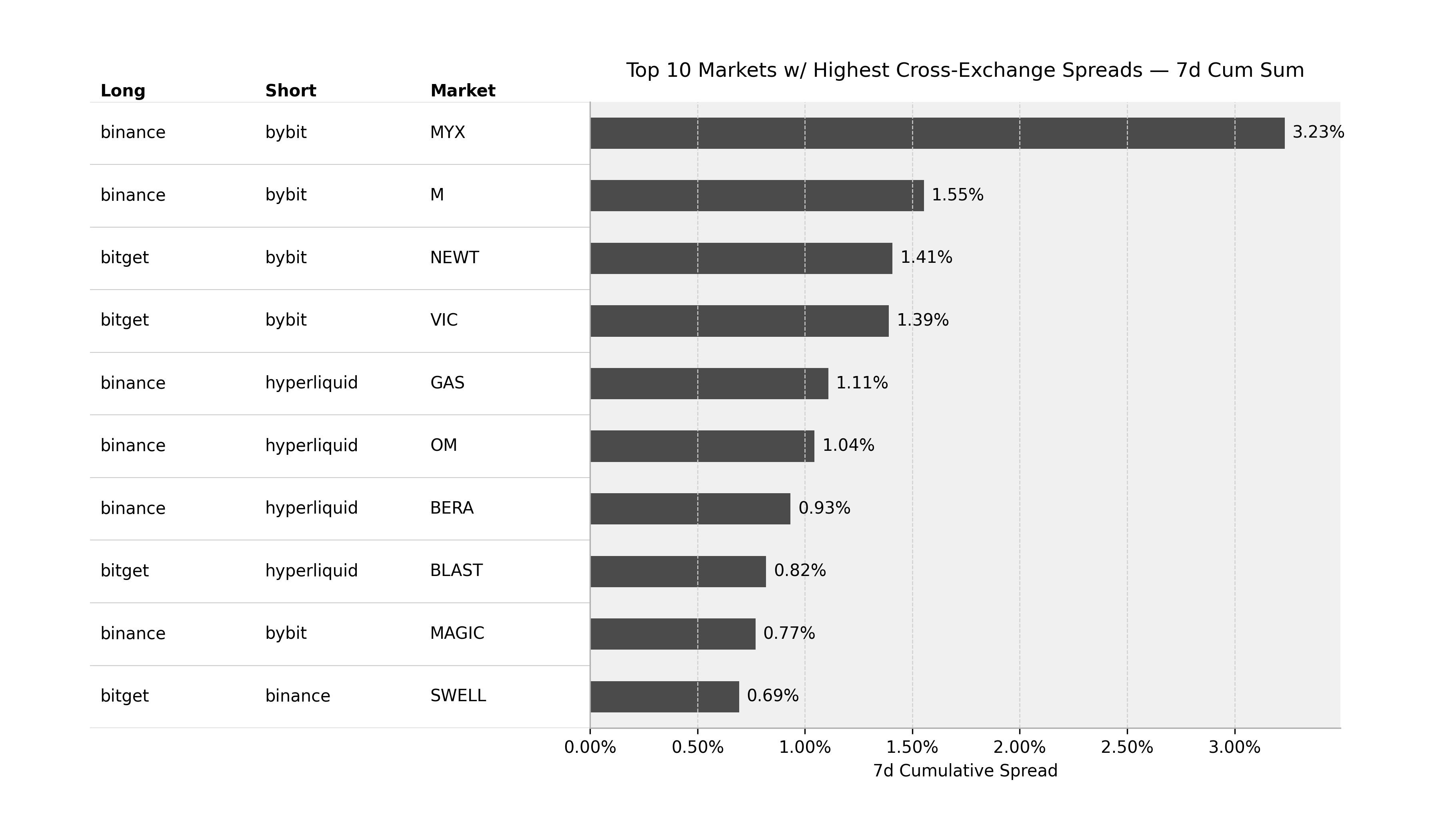

Funding Arbitrage & Market Dislocations

Cross-exchange funding differentials remained a source of alpha, offering attractive arbitrage opportunities. The most significant opportunity was identified in the MYX perpetual, with a notable 7-day cumulative spread of 3.23% available by establishing a long position on Binance and a short on Bybit. A secondary, though still compelling, spread of 1.55% was found in the M perpetual, also through a long on Binance and a short on Bybit. These spreads indicate that while the overall funding environment has cooled, pockets of inefficiency and liquidity fragmentation persist across venues, providing fertile ground for basis trading strategies.

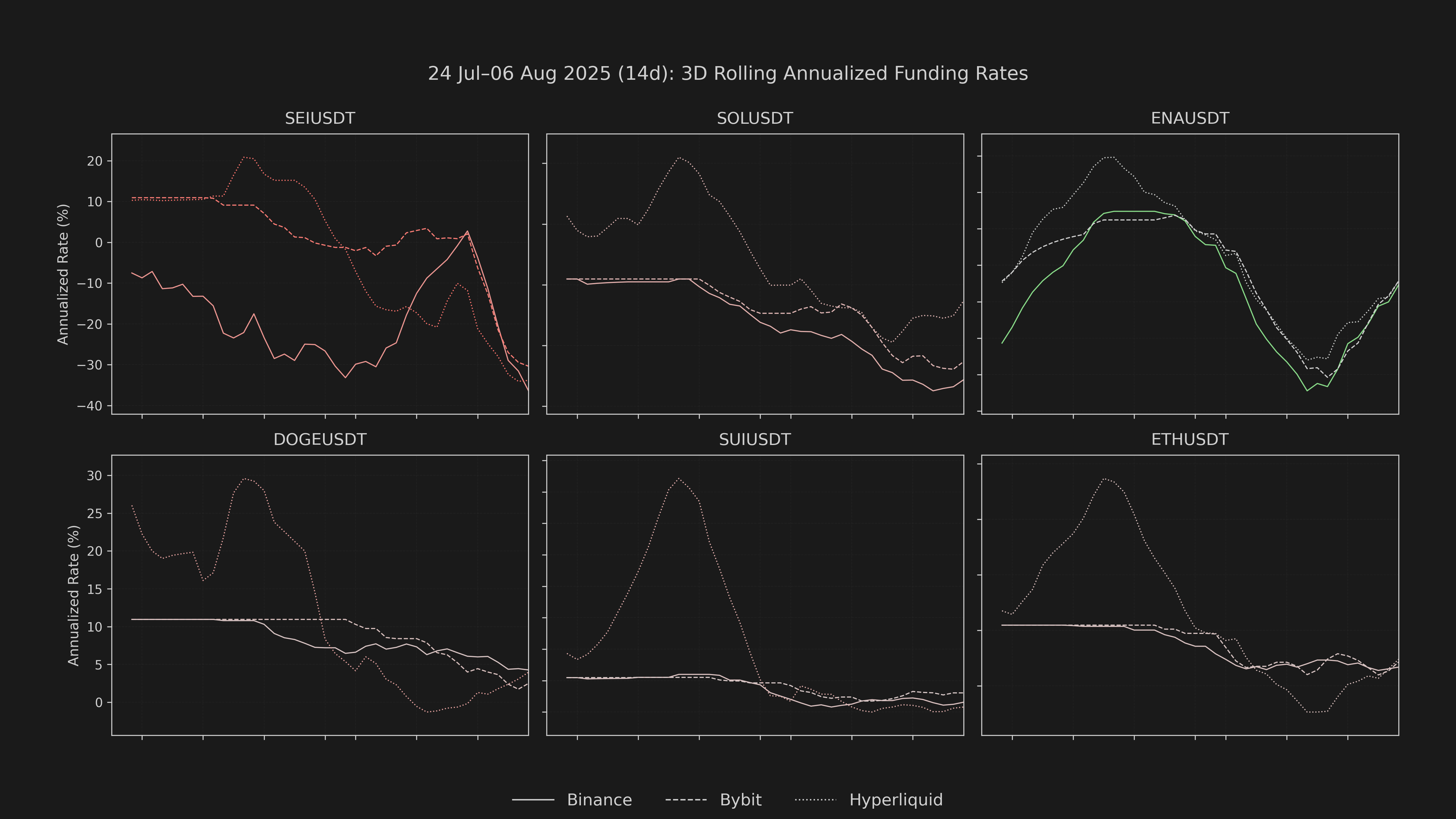

Altcoin Funding Dynamics

Funding rates within the altcoin space showed notable divergence, reflecting concentrated and idiosyncratic positioning. The SEI perpetual on Binance and Hyperliquid saw a significant decline in its 8-hourly cumulative funding rate, moving from negative to even more negative readings. This signals an intensification of short-side positioning on the asset. Conversely, the ENA perpetual on both exchanges, which was already in negative territory, saw a further decline in its funding rate, with Binance's cumulative funding moving from -0.000243 to a new negative of -0.000692, while Hyperliquid’s moved from -0.000277 to -0.000203. This reinforces the bearish sentiment and persistent short interest on ENA.

Conclusion

The current rates and basis architecture is characterized by a significant deleveraging from previously overheated levels. While this provides a more stable, less-frothy foundation for a potential market bounce, the deep backwardation in the CME basis and the lingering negative funding on certain altcoins suggest that systematic risk remains elevated, and the structure is vulnerable to further downside moves.