.png)

.png)

Weekly Recap : Crypto Rates W33

Market Overview

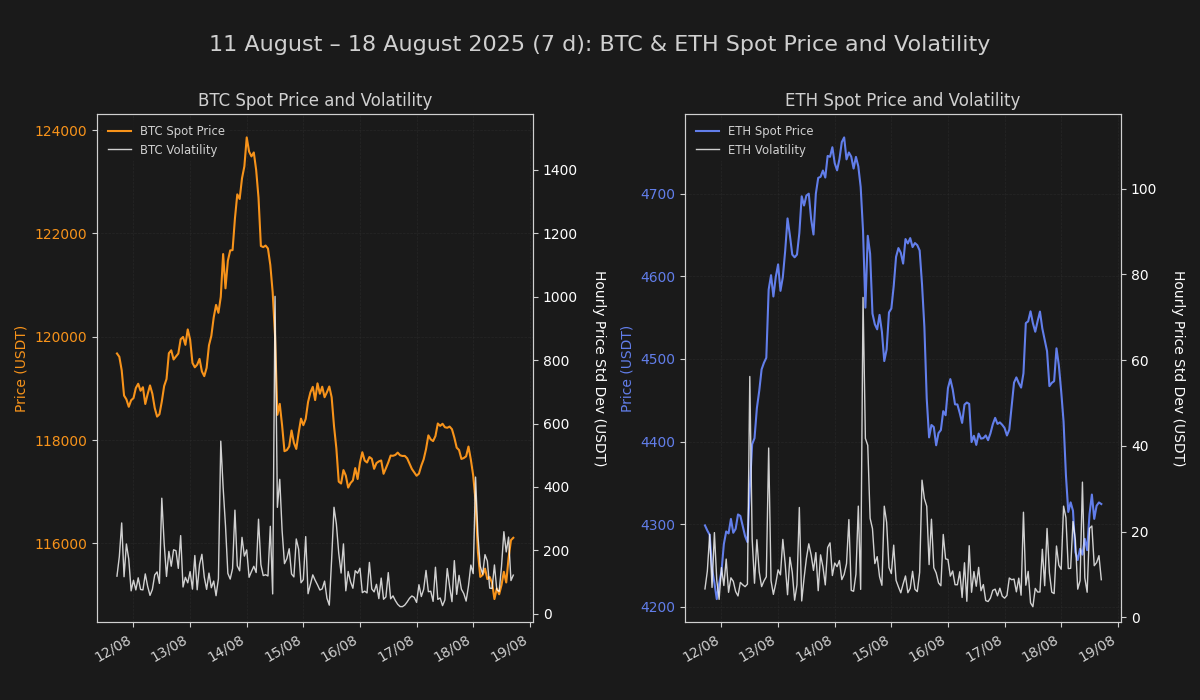

The digital asset landscape underwent a significant shift this week. After establishing a new all-time high, Bitcoin's momentum stalled, giving way to a period of consolidation and profit-taking. This correction was marked by a broad deleveraging of speculative long positions and a cooling in market-wide turnover. While institutional inflows into exchange-traded products remained robust, the overall market tone grew fragile, reflecting a dichotomy between sustained institutional demand and weakening speculative conviction.

Rates & Basis Analysis: Bitcoin and Ethereum

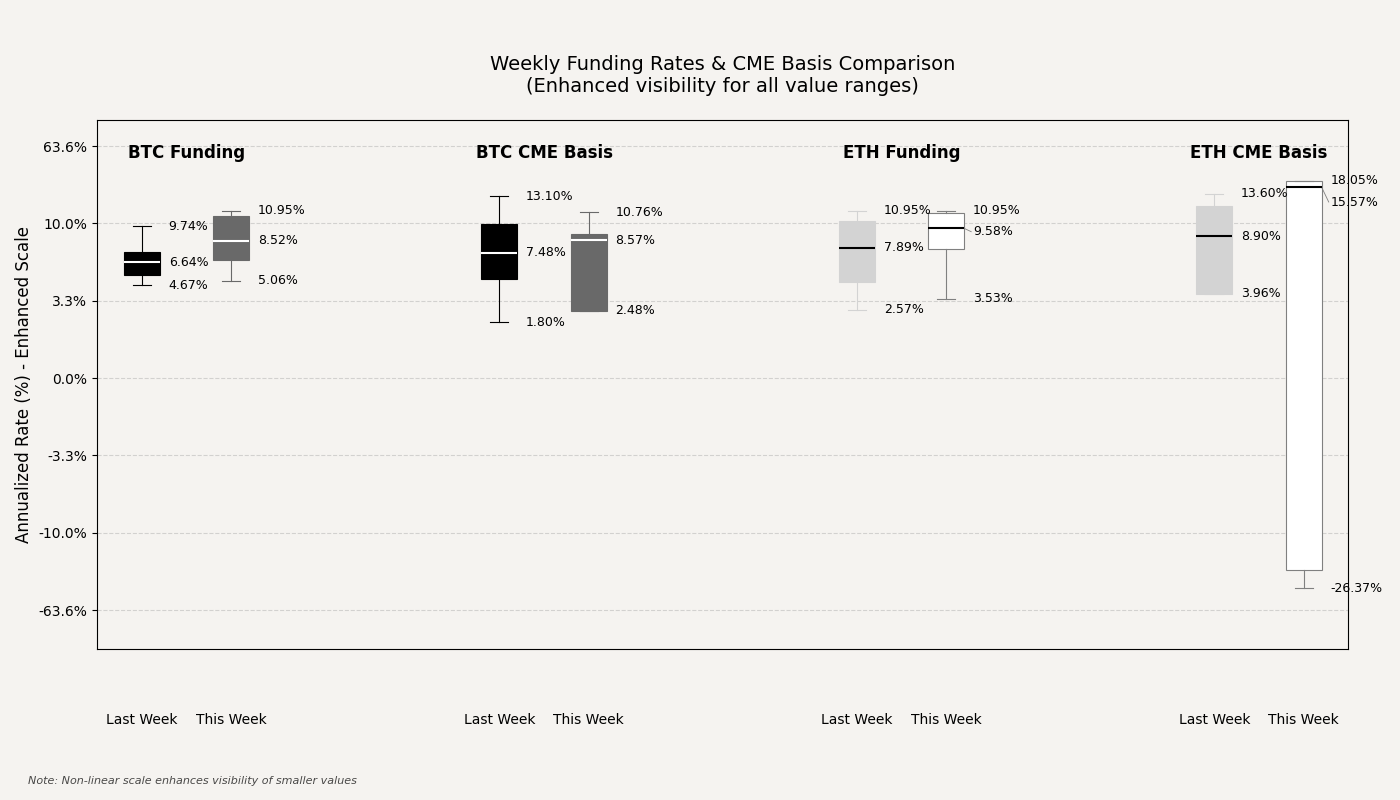

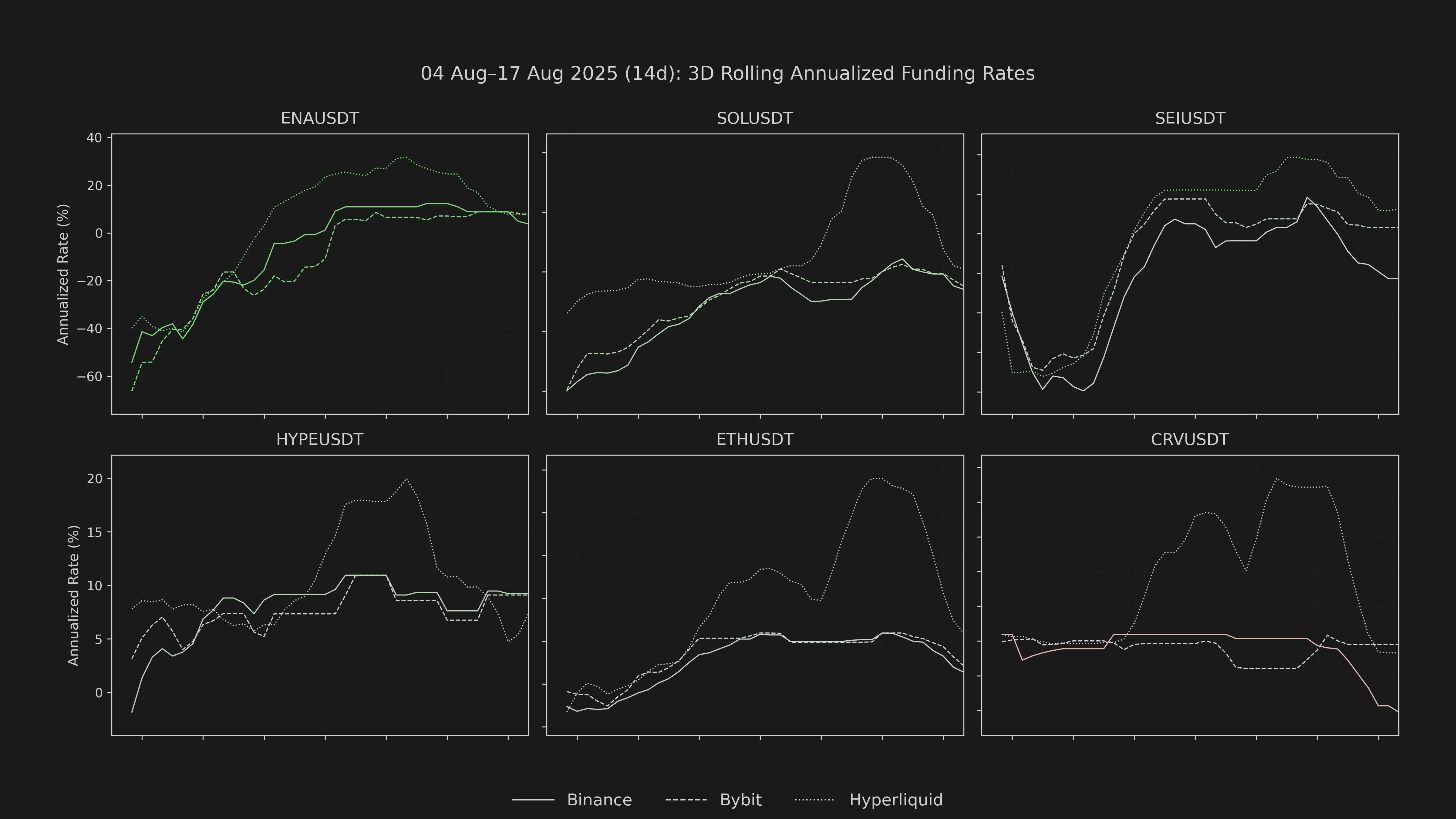

The funding rate environment for both Bitcoin and Ethereum underwent a notable expansion this period, signaling renewed bullish sentiment in the perpetual futures market. For Bitcoin, average annualized funding rates climbed from a range of 4–8% in the previous week to consistently trade above 8% this week, often hitting double-digit highs. This marks a clear tightening of carry costs for leveraged longs. Ethereum witnessed an even more pronounced shift, with average funding rates surging from low single-digit levels to also hover near or above 10%, indicating a strong, speculative long bias has returned to the market.

he term structure on the CME displayed similarly volatile characteristics. Bitcoin's basis, which averaged a healthy mid-to-high single-digit premium last week, experienced significant swings, dipping into negative territory on one occasion before recovering to trade near 10%. The spread's volatility expanded considerably. For Ethereum, the CME basis demonstrated an even more extreme range, with daily readings oscillating violently from a deep discount of over -26% to a steep premium exceeding 17%, a clear reflection of heightened uncertainty and fragmented institutional positioning.

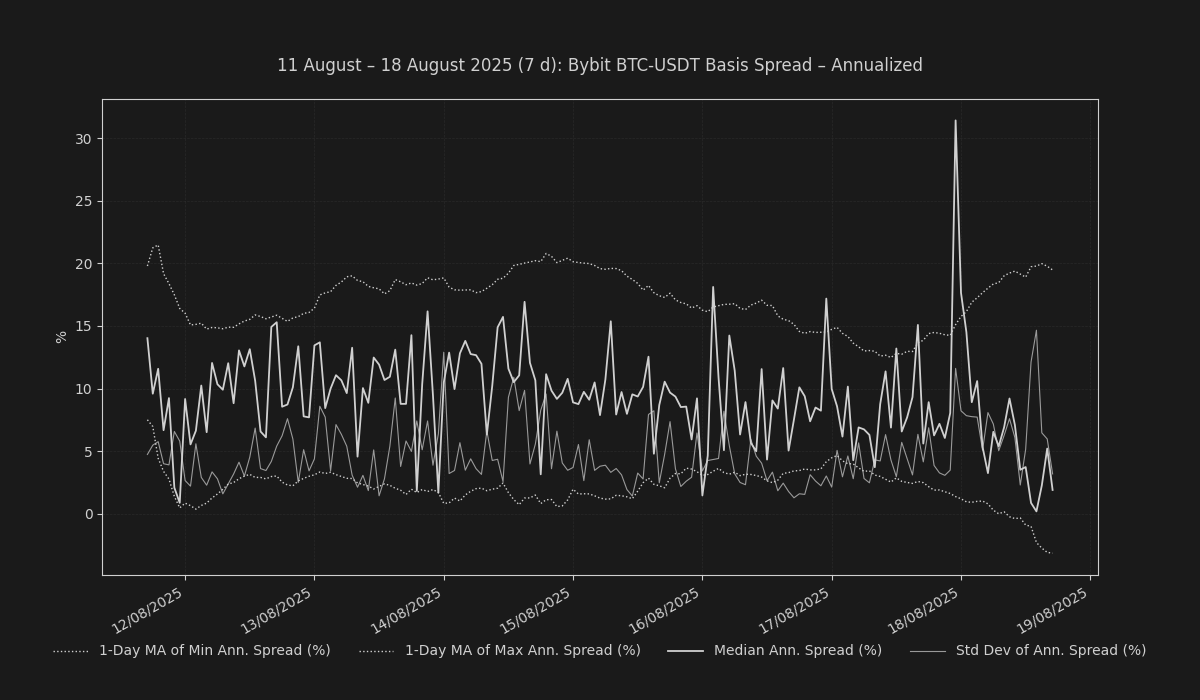

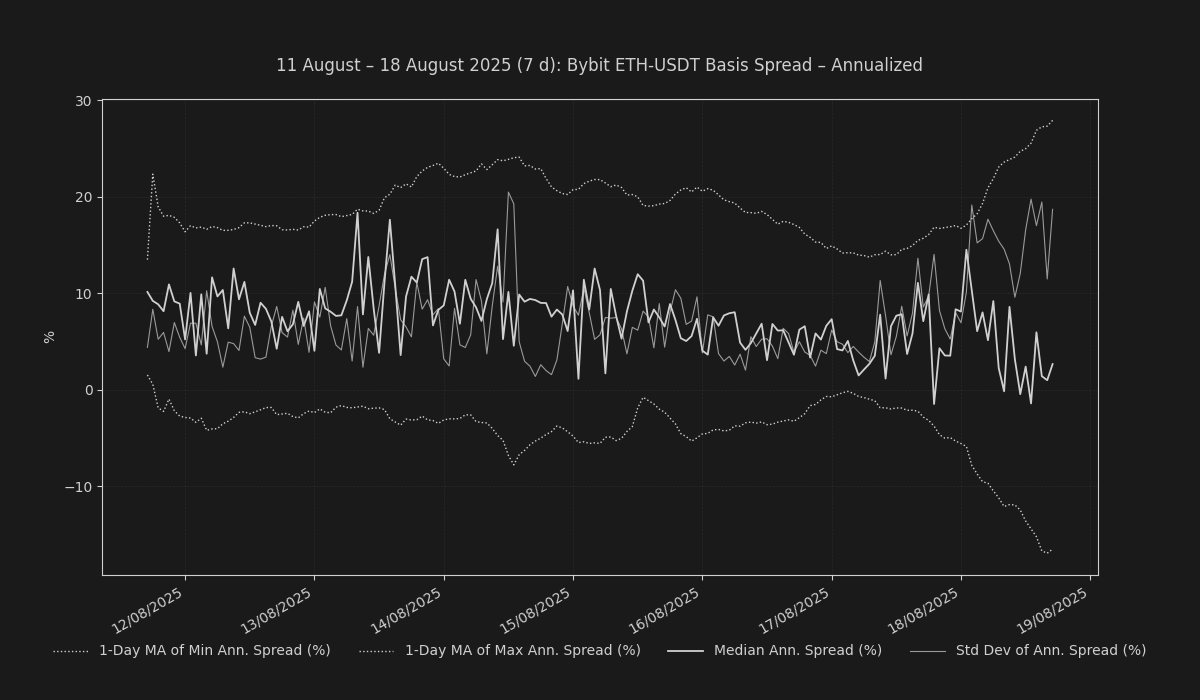

On the other hand, the offshore basis on Bybit presented a picture of compression. The annualized close for the BTC-USDT basis settled near a muted 1.89%, while the ETH-USDT basis finished in a backwardation of approximately -7.70%. This contrasts sharply with the expansion of funding rates, suggesting that while perpetual traders are paying for carry, demand for dated exposure in offshore venues has not kept pace, resulting in a flattening or inversion of the forward curve

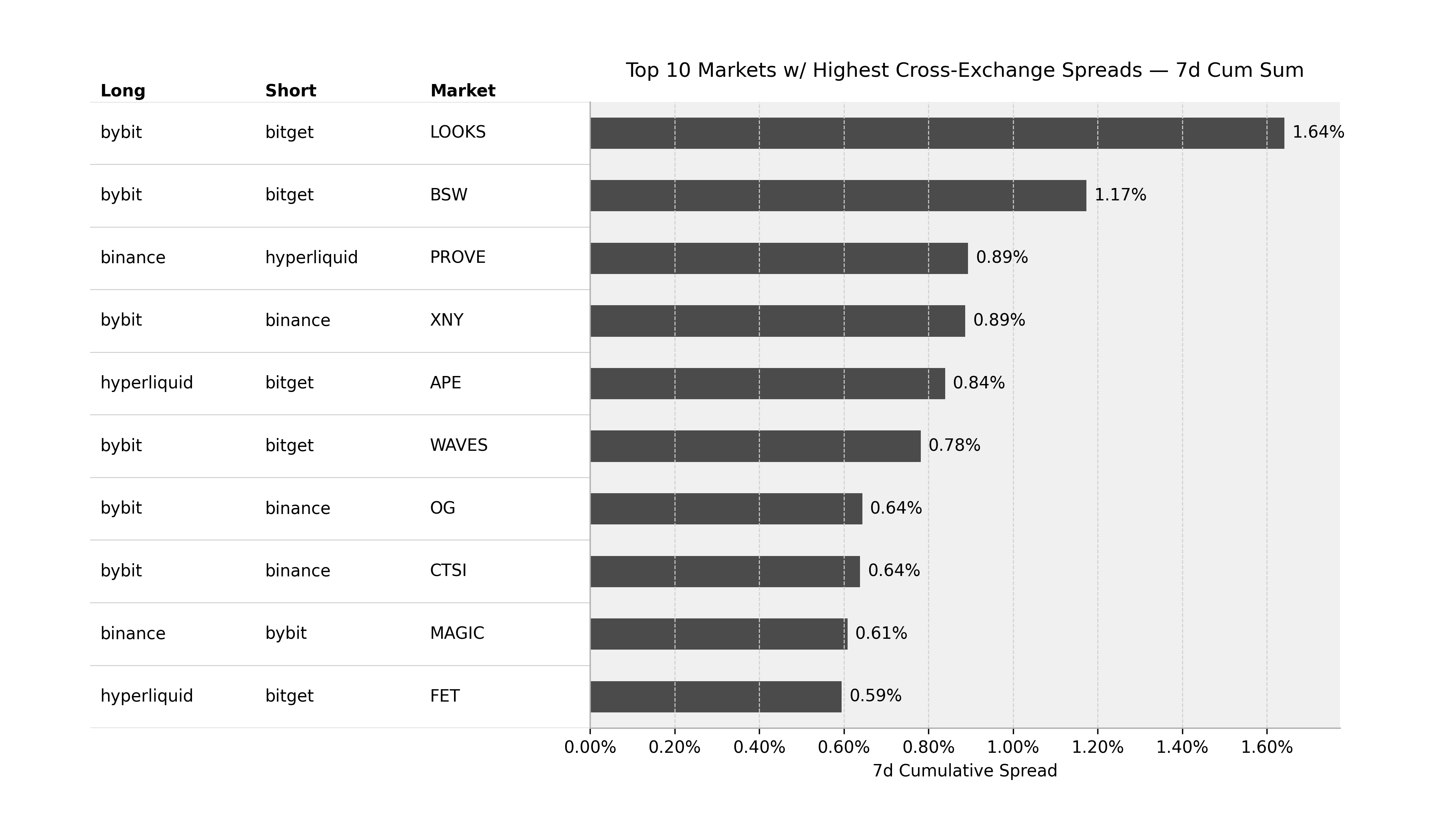

Funding Arbitrage & Market Dislocations

Select cross-exchange differentials persisted, offering compelling tactical carry opportunities. The most significant dislocation was observed in LOOKSUSDT, where a long position on Bybit paired with a short on Bitget would have yielded a cumulative spread of roughly 1.64% over the week. Another notable opportunity was found in BSWUSDT, with the same long Bybit/short Bitget pair producing a 1.17% cumulative spread. These elevated spreads highlight persistent liquidity imbalances and venue-specific sentiment skews.

Altcoin Funding Dynamics

Within the broader altcoin complex, funding dynamics were divergent. On Binance, TRXUSDT funding flipped decisively from a positive close in the prior week to a negative close this week, signaling a sharp increase in short-side conviction. Conversely, the cumulative funding for SEIUSDT on the same exchange saw a notable positive uptick, moving from a near-zero close to a more pronounced positive reading. These contrasting moves underscore the idiosyncratic nature of altcoin flows, which often act independently of major market sentiment.

Conclusion

The rates environment this week reflects a return to a more aggressive, though highly volatile, speculative stance. The broad-based tightening of perpetual funding indicates that leveraged long positioning is expanding despite a sharp price pullback. The significant divergence between funding rates and the more muted or backwardated basis in term futures suggests that market conviction is primarily concentrated in the perpetual space. This configuration presents a fertile ground for sophisticated basis trading and funding arbitrage strategies but also hints at fragile market structure susceptible to further deleveraging events.