.png)

.png)

Weekly Recap : Crypto Rates W30

Market Overview

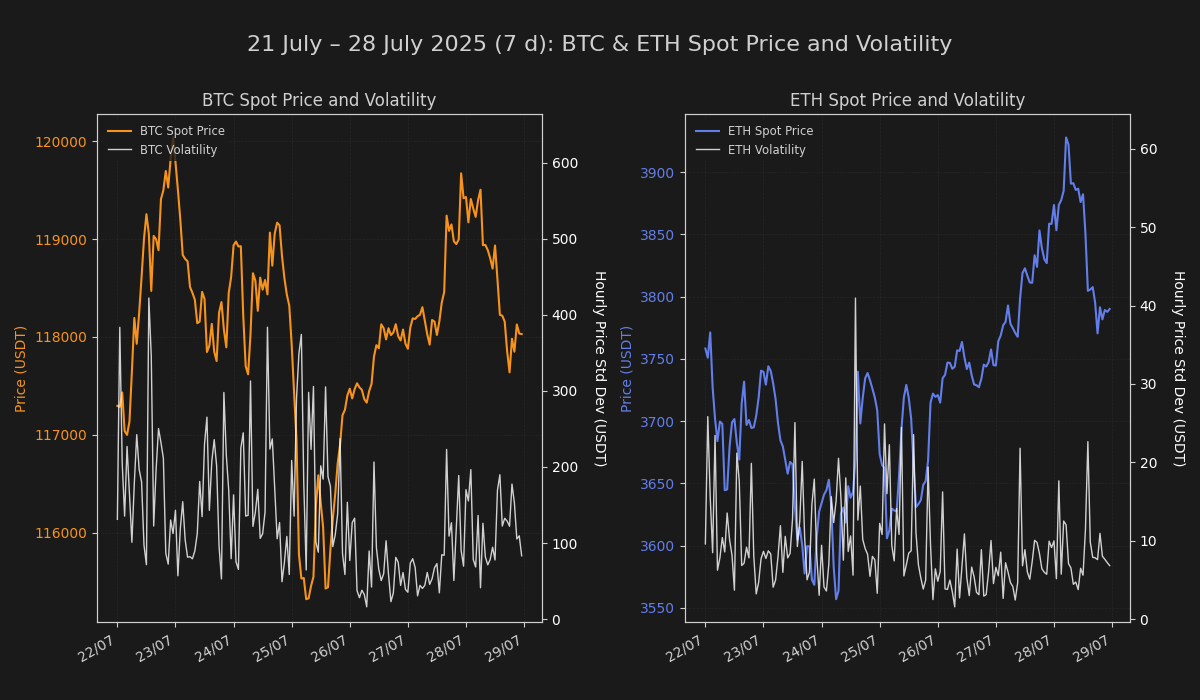

Digital asset markets entered a period of reassessment after the recent price rally stalled, with price action characterized by a mild pullback from the all-time high. This consolidation phase has been marked by a broad cooldown in speculative activity, even as certain on-chain metrics and capital flows suggest a resilient underlying bid. The market is now absorbing prior gains, with mixed signals emerging across key sectors as participants gauge the potential for a renewed uptrend.

Rates & Basis Analysis: Bitcoin and Ethereum

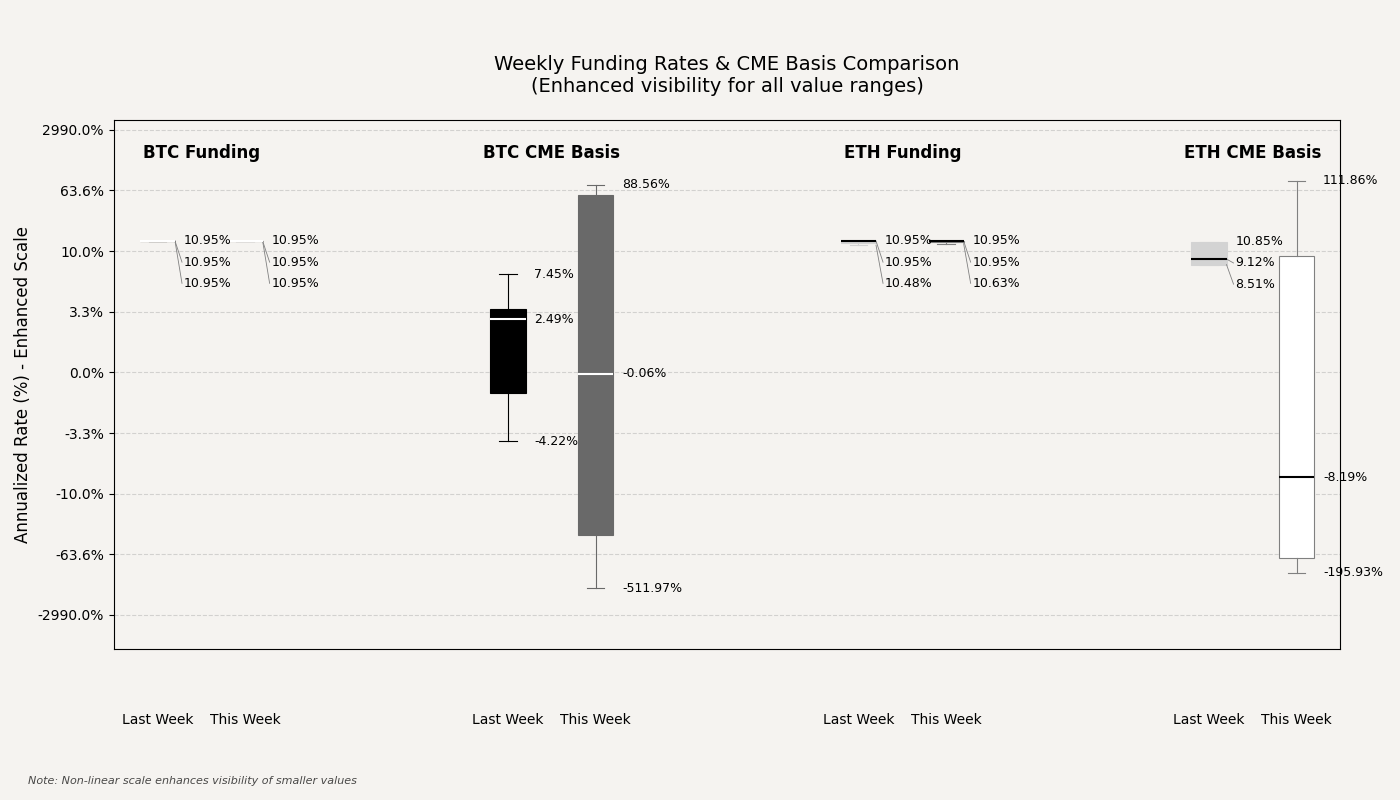

The cost of leverage in the perpetual swap market experienced a slight compression, indicating a marginal cooling of speculative fervor. Bitcoin's annualized funding rates eased to an average of approximately 10.90% this week, a minor decline from the prior period's steady 10.95%. Similarly, Ethereum's perpetual funding rates also saw a minor downtick to roughly 10.85% from 10.88%. This subtle narrowing of funding costs suggests that while a structural demand for long-side exposure remains, the acute premium for leverage has slightly moderated in the wake of the price retracement.

In the regulated futures market, the CME basis for both Bitcoin and Ethereum experienced a severe and sudden contraction. The annualized CME basis for Bitcoin shifted dramatically from an average of roughly 1.69% in the prior week to a deeply negative average of approximately -68.92% this week, while Ethereum's basis underwent an equally violent move, collapsing from an average of about 16.81% to -45.57%. This extreme volatility and flip to a steep backwardation in the regulated market points to a significant institutional deleveraging event or intense repositioning of hedging overlays, temporarily breaking the typical contango structure and creating a substantial dislocation between regulated and offshore venues.

Offshore, the CEX (Bybit) futures basis for Bitcoin closed the week at a robust 13.26%, suggesting a healthy contango. In contrast, the Ethereum basis on the same venue closed at -2.05%, indicating a slight backwardation. The divergence in basis between the two major assets hints at a lack of uniform conviction across the complex, with distinct risk appetites for Bitcoin versus Ethereum.

Funding Arbitrage & Market Dislocations

Cross-exchange funding rate differentials remained elevated, presenting compelling arbitrage opportunities for market participants. The most attractive dislocation was identified in the NEWT perpetual, which offered a significant 7-day cumulative spread of 4.64% by pairing a long position on Binance with a short position on Bybit. A secondary, though still substantial, opportunity was found in the ZORA market, with a cumulative spread of 2.75% achievable through a long position on Bitget and a short position on Hyperliquid. These persistent spreads underscore a continued fragmentation of liquidity and differential risk pricing across various crypto venues.

Altcoin Funding Dynamics

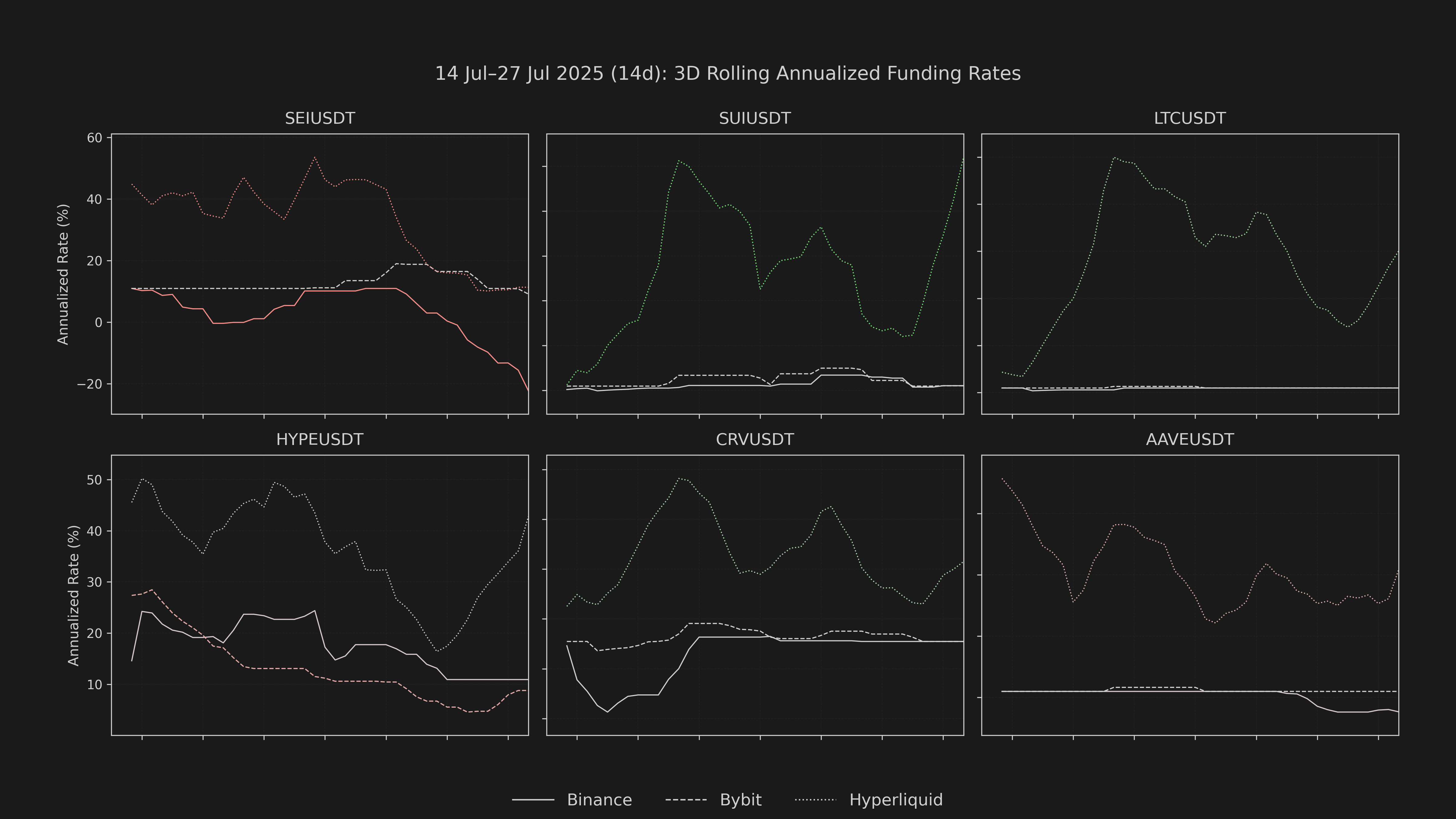

Within the broader altcoin landscape, specific assets showed notable shifts in their funding rate trajectories, reflecting concentrated speculative positioning. The SEI perpetual on Binance experienced a pronounced negative shift, with its 8-hourly cumulative funding rate moving from a positive reading to a negative -0.000451, indicating a sharp increase in short-side interest on that venue. Conversely, the SUI perpetual on Hyperliquid showed an opposite trend, with its cumulative funding rate surging from a prior week's reading of 0.00031 to a robust 0.000885, a significant positive expansion that highlights a pocket of strong speculative demand.

Conclusion

The current rates architecture is characterized by a high degree of tension, with a stable but slightly compressing perpetual funding backdrop coexisting with unprecedented volatility in the regulated term structure, suggesting a market where underlying structural longs are being held, but systematic risk capacity is constrained and vulnerable to rapid, episodic shocks.