.png)

.png)

Weekly Recap : Crypto Rates W41

Market Overview

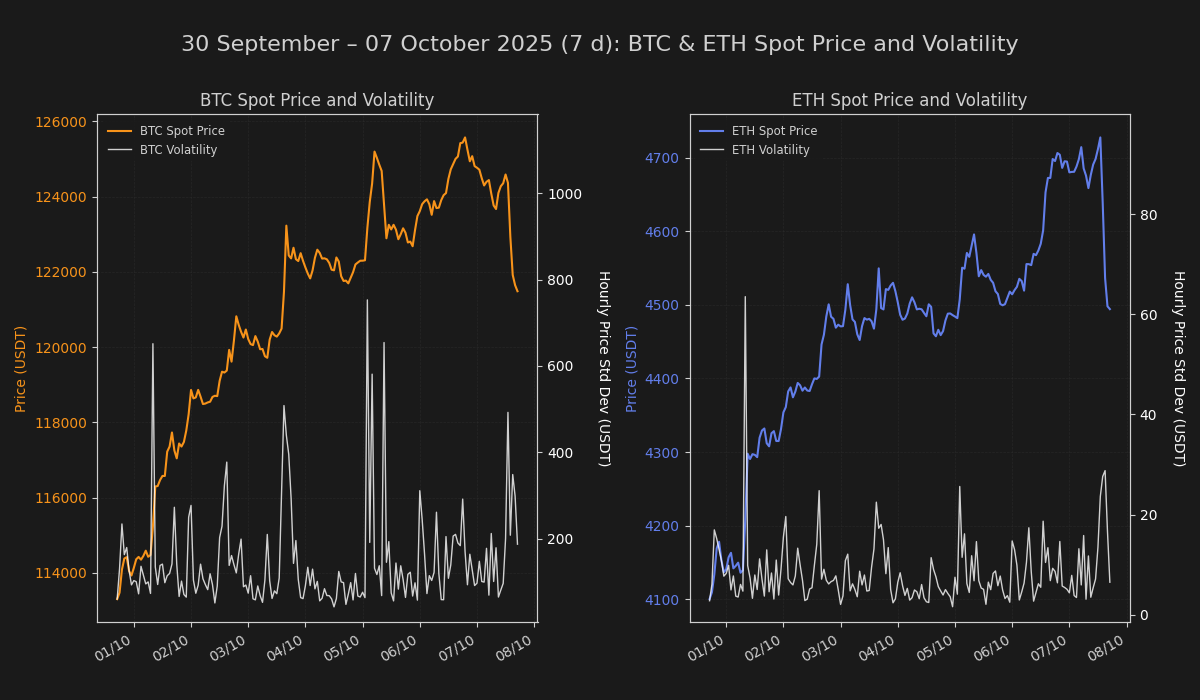

Bitcoin's ascent to new all-time highs near $125.5K has been accompanied by a pronounced tightening of financing conditions across derivative markets. The move reflects a material shift in positioning dynamics, with leveraged long exposure expanding in tandem with improved institutional participation and strengthening on-chain fundamentals.

Rates & Basis Analysis: Bitcoin and Ethereum

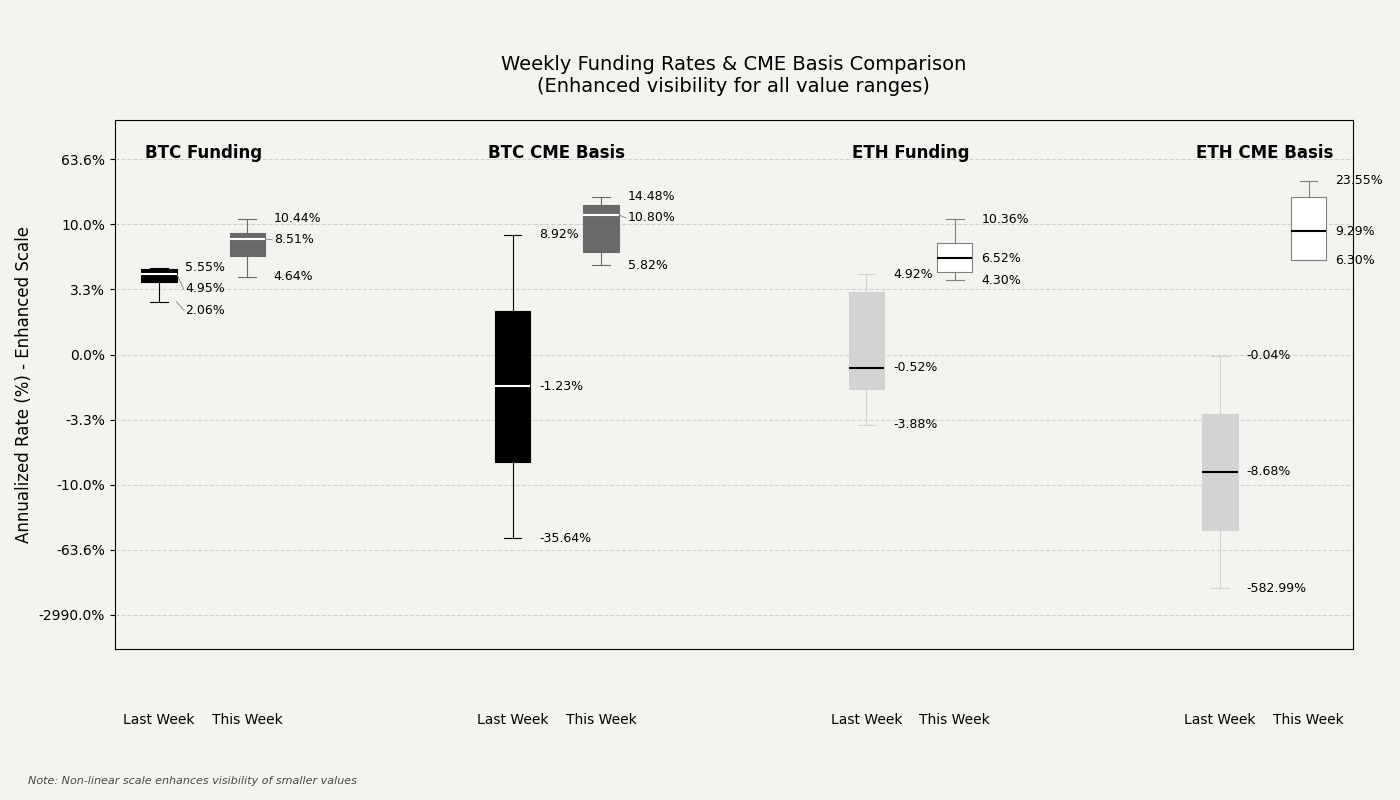

The trajectory of perpetual swap financing has undergone a decisive shift toward more expensive carry costs. Bitcoin perpetual funding rates experienced a notable expansion, with average annualized levels climbing to approximately 7.9% during the period, up from roughly 4.5% in the preceding week. This marks a reacceleration in long-side financing costs, with daily observations ranging from 4.6% to 10.4%, indicating sustained willingness among participants to pay for directional exposure.

Ethereum financing exhibited an even more pronounced adjustment. Average annualized funding rates advanced to approximately 6.2%, a sharp reversal from the prior week's subdued 0.6% average, which had included several instances of negative funding. The current period saw daily readings spanning from 0.1% to 10.4%, with the funding environment transitioning from mixed sentiment to uniformly positive carry costs. This realignment suggests a broad unwinding of short-side positioning alongside renewed speculative interest.

The CME futures basis landscape presented a starkly different picture compared to the prior period's dislocations. Bitcoin's annualized term premium stabilized around 10.1%, with daily observations ranging from 5.8% to 14.5%. This represents a marked normalization from the prior week's erratic behavior, which had oscillated between deeply negative and modestly positive territory. The current elevated and consistent premium indicates renewed institutional demand for dated exposure, with term buyers willing to pay meaningful carry.

Ethereum's CME basis displayed a similar recovery in structure. After experiencing extreme backwardation in the previous period—including an outlier reading approaching -583%—the basis normalized to average approximately 10.5%, with daily observations from -1.0% to 23.6%. The term structure's stabilization at elevated levels reflects a recalibration of institutional positioning, with forward curve premiums now commanding significant compensation for duration risk.

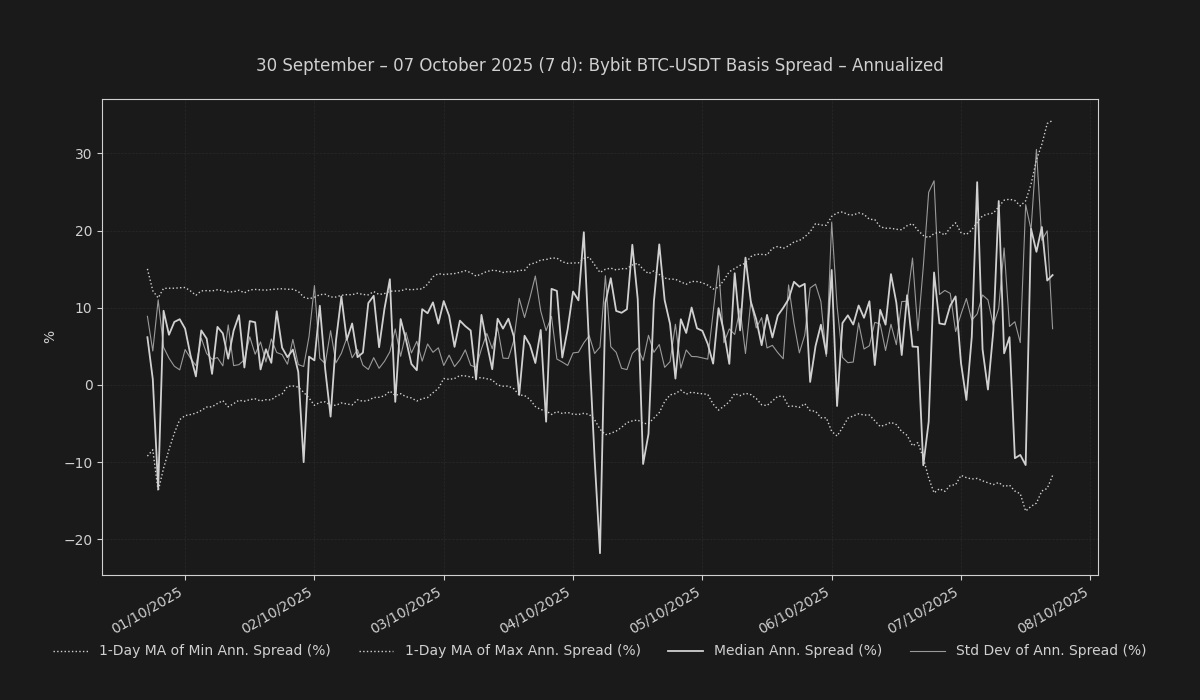

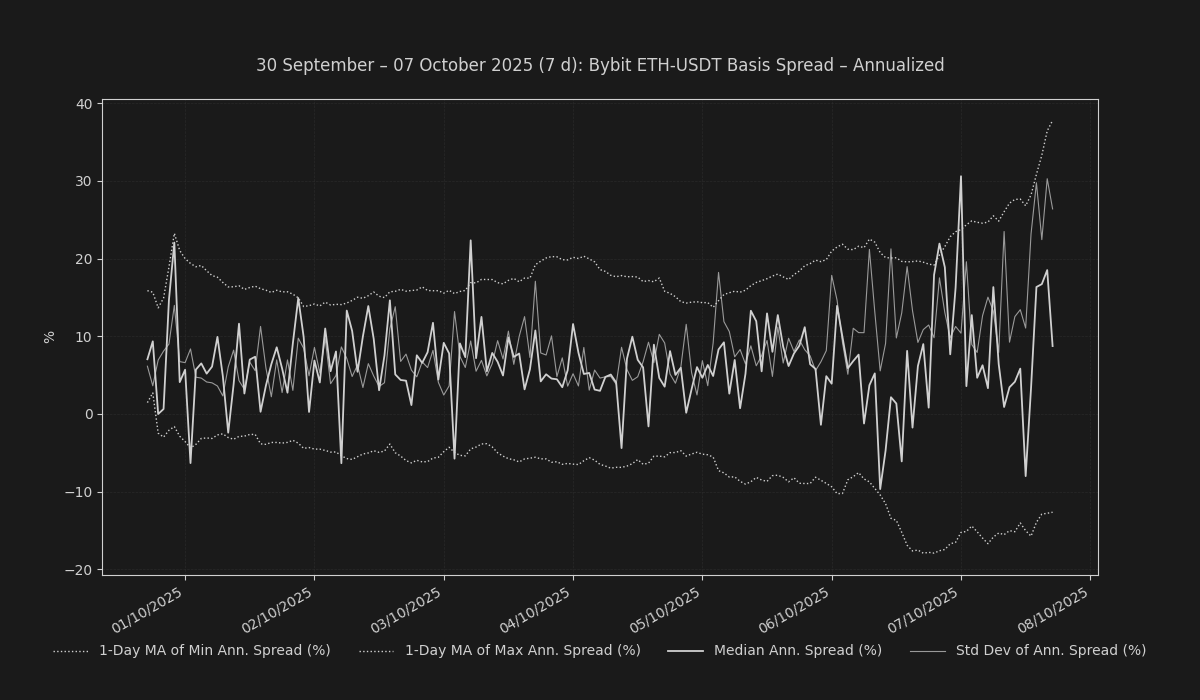

The Bybit term structure for Bitcoin closed the observation period at an annualized premium of 18.4%, reflecting substantial demand for forward-dated BTC exposure on offshore venues. Ethereum's Bybit basis settled at 15.3%, maintaining a meaningful premium despite earlier period volatility. Both assets exhibited elevated basis volatility as measured by standard deviations above 10%, suggesting active repositioning and price discovery in the term structure. The convergence of elevated CME and offshore basis levels indicates a synchronized tightening of financing conditions across market segments, with term buyers competing for exposure across geographical and regulatory venues.

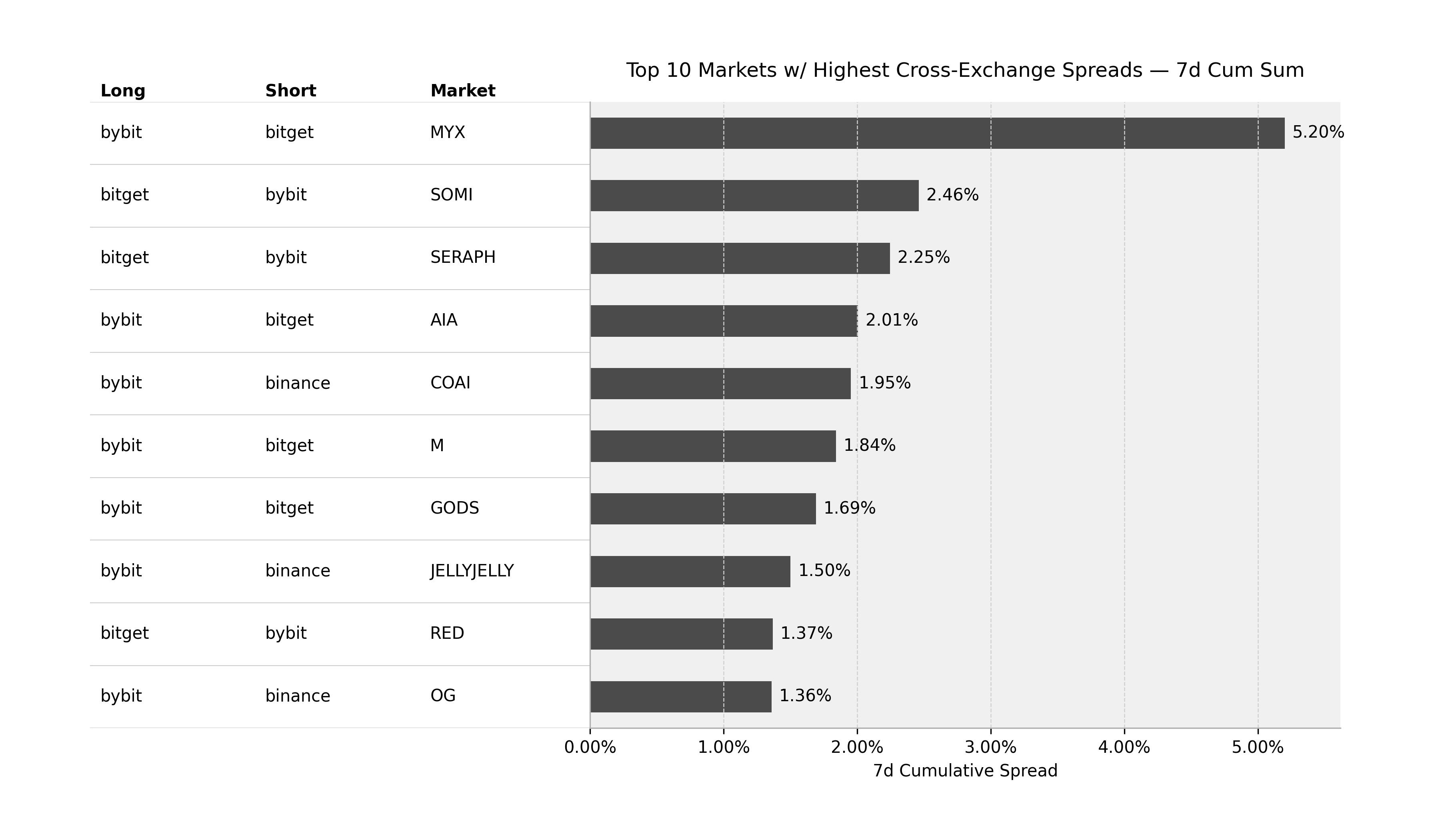

Funding Arbitrage & Market Dislocations

Persistent pricing inefficiencies across exchanges continue to present actionable opportunities for basis capture. The most compelling dislocation emerged in the MYX perpetual market, where a paired position—long Bybit versus short Bitget—would have captured a cumulative funding spread of approximately 5.2% over the seven-day observation window. This magnitude of cross-venue divergence points to segmented liquidity pools and heterogeneous participant positioning across platforms.

A secondary opportunity was observed in the SOMI market, where a long Bitget exposure hedged against a short Bybit position yielded a cumulative spread of 2.46%. The SERAPH market similarly displayed notable cross-exchange pricing friction, with a long Bitget versus short Bybit strategy accumulating 2.25% over the period. These structural inefficiencies underscore the fragmented nature of altcoin liquidity, where venue-specific order flow dynamics create persistent basis capture opportunities for cross-platform arbitrageurs.

Altcoin Funding Dynamics

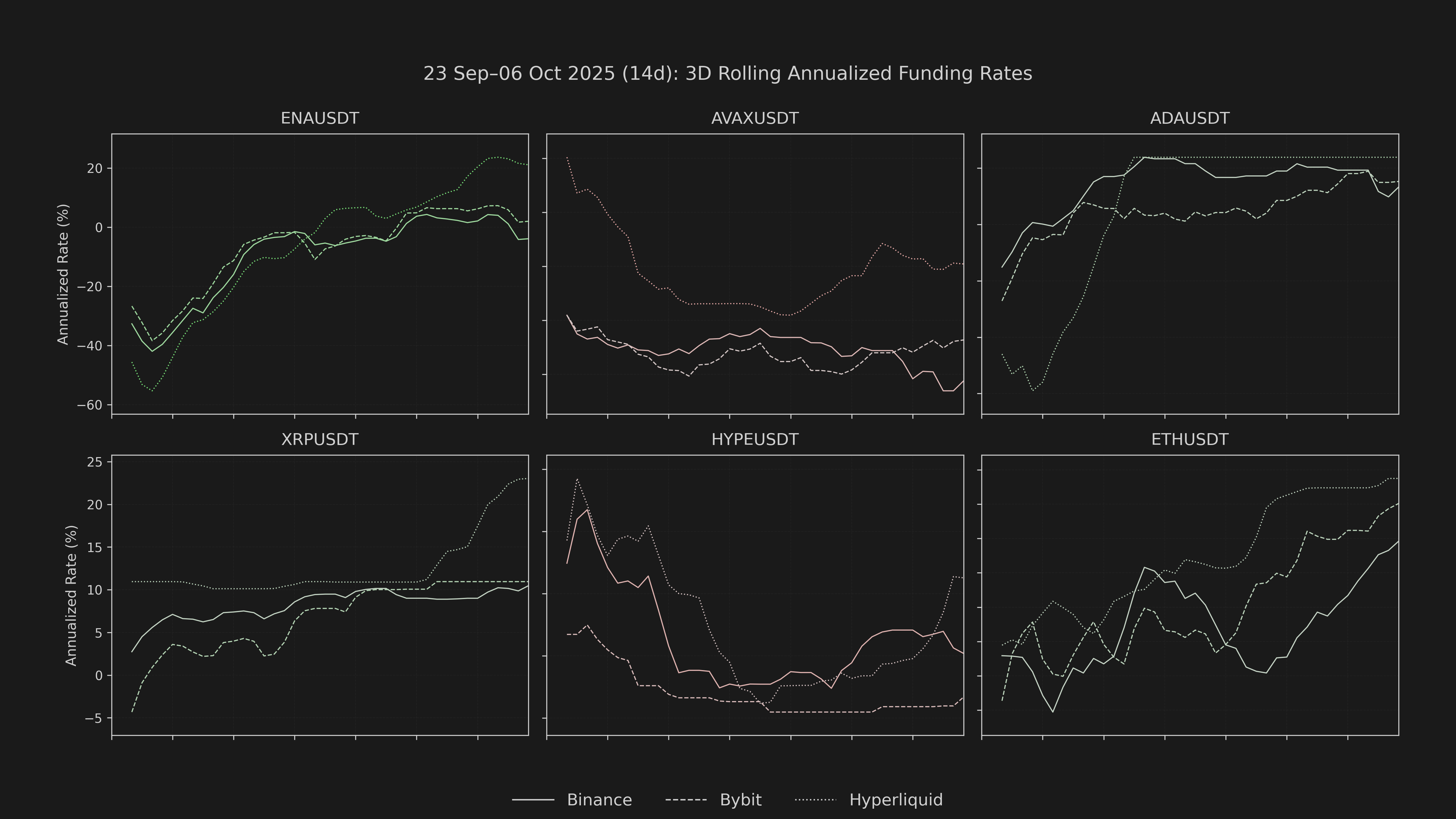

Sentiment within the altcoin sector was highly varied. Funding for ENA on Binance underwent a notable reversal, shifting from a negative footing in the previous week to firmly positive territory, suggesting short covering or a renewal of bullish speculation. Conversely, sentiment for SOL on Bybit deteriorated, with its funding rate flipping from positive to negative, indicating an increase in bearish sentiment or hedging activity.

Sentiment shifts within the altcoin complex revealed divergent positioning trends. HYPE perpetuals on Binance experienced a material re-rating, with 8-hourly funding sums nearly doubling from 0.000126 to 0.000249, signaling a significant escalation in long-side demand. This acceleration reflects either speculative accumulation or short-side capitulation following the broader market's upward trajectory.

TRX displayed one of the more dramatic sentiment reversals, with Binance funding flipping from deeply negative territory at -0.000108 in the prior period to capped positive at 0.0001 currently. This swing from net short to net long bias indicates a wholesale repositioning in the asset, likely driven by either fundamental catalysts or technical breakouts that triggered stop cascades.

Conversely, SOL funding on Binance transitioned from negative -0.000074 to modestly positive 0.000054, suggesting a more measured shift in positioning. The move from contango to backwardation reflects easing short pressure rather than aggressive long accumulation. Similarly, ETH funding on Binance normalized from negative -0.000035 to the ceiling of 0.0001, aligning with the broader strengthening of major asset financing rates.

Conclusion

The financing landscape across digital assets has undergone a material repricing, with both perpetual and term markets commanding elevated carry costs. The convergence of tightening CEX funding rates, normalized CME term premia, and elevated offshore basis levels suggests a market operating with increased leverage and directional conviction. This environment presents favorable conditions for carry strategies while signaling that speculative positioning has expanded meaningfully in conjunction with spot demand, warranting close monitoring of leverage metrics as the rally matures.